Online Lending: Friend or Foe of Community Bankers?

As new online-lending platforms change the small-dollar lending land- scape, opportunities may exist for community banks.

{kind=link}

Community banks have long been the go-to source for small-dollar loans.[1] Because they frequently interact with local borrowers, they develop a good sense of which loans are good risks. Close ties to borrowers allow them to issue small loans with a high degree of confidence that they will be paid back.

Unfortunately, smaller loans are more costly for banks to originate and service than larger loans because they require the same resources to approve as more-remunerative loans. As a result, many community banks have moved upmarket. Meanwhile, large institutions use credit card products to provide credit to borrowers looking for loans of less than $100,000. But they don't provide education on the proper use of credit, and borrowers often learn the hard way that attractively low minimum payments may keep them from reducing the actual debt.

Today, there's a shift as new players enter the lending arena through the Internet. Online credit platforms are disrupting the market, issuing increasingly greater volumes of small consumer and business loans. Online lenders offer a streamlined application process, expeditious decisions, and quick disbursal of funds. What's more, customers have proved willing to pay higher interest rates for online speed and convenience. New players often complete the loan process in four human interactions, compared with up to 14 at traditional banks. The automated decision making screens out inappropriate applications, and the automated closing and funding process reduces costs to close and store loan notes.

Companies such as Prosper and Lending Club led the way with peer-to-peer lending, which used credit platform technologies to provide personal loans to individuals. Nowadays, small business owners have easier access to credit from platforms meant for them-for example, OnDeck Capital, Endurance Lending Network, IOU Central, Fundation, QuarterSpot, and CapTap.

Market Growth

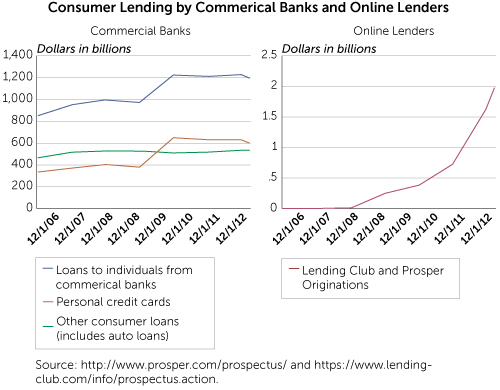

One of the most striking aspects of online lending is how rapidly it has grown. Kabbage, an online lender launched in May 2011, grew by 298 percent from 2012 to 2013. Lending Club, which originated $1.18 billion from 2007 to 2012, expects to originate an additional $4 billion in 2014 alone. OnDeck Capital is growing more than 100 percent annually. A comparison of the growth of Prosper's and Lending Club's originations with the growth of commercial bank loans to individuals during the same period is striking. (See "Consumer Lending by Commercial Banks and Online Lenders." )

The Federal Reserve Bank of New York's 2013 Small Business Credit Survey shows a market demand for credit products of less than $100,000. Fifty-one percent of respondents sought a loan of under $100,000.

As of March 31, 2013, FDIC-insured depository institutions listed a cumulative total of $285 billion in commercial and industrial small-business loans of under $1 million, with 43 percent of the volume for amounts less than $100,000. Eighty-three percent of those loans are held by commercial banks. Of those, four out of five are held by institutions with more than $1 billion in assets.[2]

As large traditional banks have fed a need for personal loans and business loans by offering credit cards without credit education, consumers have racked up large balances. Now many are seeking out companies like Lending Club to refinance credit card debt. Credit card balances at FDIC depository institutions totaled $660 billion as of March 31, 2013, an 86 percent increase over the first quarter of 2007.[3]

Cost Comparison

Online lending has both advantages and disadvantages when it comes to costs. Lender operating costs, including underwriting, are much lower than at traditional financial institutions. Online lenders do not have to maintain brick-and-mortar branches, and many employ high levels of automation for applicant screening.

Even though online lenders have lower costs, it is generally more expensive for borrowers to obtain credit through online platforms. That is largely because online lenders use broad, risk-based pricing models, which result in only the most creditworthy borrowers obtaining rates that are better than what they could get at a traditional bank. The average interest rate is 16.97 percent at Lending Club and 19.31 percent at Prosper, with the difference likely attributable to the different risk profiles of their customers.[4] It's worth noting, however, that the rates do not take into account origination fees, which would make the annual percentage rates slightly higher.

Regulatory Environment

The regulatory environment for online lending is still evolving. There's some lack of clarity as to which regulator should oversee it. The Securities and Exchange Commission provides oversight on the investor side, while state-level bank regulators govern online lenders in the states in which they do business. There may also be oversight by the FDIC or the Federal Reserve if online lenders have partnerships with banks. In addition, the Consumer Financial Protection Bureau has announced plans to provide oversight and regulation in the near future.[5] Bankers who were interviewed for this article cited lack of regulatory clarity as a barrier to their participation in online lending.

Lower-Income Borrowers

The growth of online lending could have positive implications for low- and moderate-income (LMI) borrowers, especially as traditional banks enter the arena. Recent research shows that lower income tends to be associated with lower credit scores.[6] As online algorithms develop further, nontraditional criteria can be incorporated to provide a better prediction of a customer's ability to pay.

The major benefit of online lending for LMI borrowers is that it dramatically reduces service costs. As traditional banks become more involved in online lending, the overall cost of funds will decline. Those two factors should increase available credit and bring down costs for both lenders and borrowers.

Currently, many lower-income individuals turn to payday loans or pawnshops for loans, sources that generally carry high fees and interest rates. Payday loans are particularly notorious for trapping customers in repeated borrowing cycles with fees that end up equaling triple-digit implied annual percentage rates. In contrast, online loans offer longer terms and lower costs, relatively speaking. Moreover, because of the various constituencies they serve, online loans are transparent in disclosing their costs, and their speed and convenience competes with high-cost alternatives.

In another development that could benefit low-income borrowers, some online lenders have expressed interest in partnering with community development financial institutions to expand credit access to underserved individuals and small businesses.

Options for Bank Involvement

Common sentiment among community banks is that small loans are no longer cost effective. But that is not always true. Small loans are not cost effective for community banks under their current origination methodology, but banks may be able to overcome that drawback by forming partnerships with online lenders. There are several ways a bank could do so:

Referrals - Community banks could refer to an online lender loans that fall outside their underwriting criteria. Such referrals would allow banks to continue their customer relationships while gaining fee income.

Onsite kiosks - Community banks could invite online lenders to set up in-branch kiosks. Borrowers who don't fit the bank's criteria would simply be referred to the kiosk.

Investment - Community banks could invest in pools of loans or provide capital to online lenders.[7]

Loan purchases - Community banks could purchase loans directly from an online lender, then pay the online lender a servicing fee.

White-label partnerships - An online lender could be asked to white label its technology platform in the name of a partner community bank.[8] The online lender would originate and service the loans, while the bank would purchase any loan that meets its criteria.

Software licensing - Community banks could license the underwriting technology and incorporate it into their systems.

Some such partnerships are already evident in the marketplace. Lending Club, for instance, has entered into partnerships with two community banks, Titan Bank in Texas and Congressional Bank in Greater Washington, DC.[9] Both banks are acting as investors, purchasing loans originated by Lending Club. In addition, Titan Bank is planning to use the Lending Club platform to service loans. The former tactic gives the banks an outlet for their capital, the latter a means of underwriting loans that would be too costly otherwise.

Online credit platforms are disrupting traditional lending markets in ways that have the potential to transform the lending business. They have removed costs from origination and servicing, while bringing enhanced data-gathering techniques to underwriting. In the absence of a lot of regulation, a disjointed market has evolved that allows many different models to be explored.

Community banks have choices to stay competitive. They may add efficiency to their current processes or integrate an online credit platform into their operations. Banks should tread slowly in the online market, however, first perfecting their underwriting methodology, then expanding to serve a broader customer base.

The biggest benefit of having banks in the online lending arena is that they can access lower-cost capital and bring down the overall cost of borrowing.

Richard D. Olson Jr. is senior vice president of retail banking at Randolph Savings Bank in Randolph, Massachusetts. Contact him at rolson@randolphsavings.com.

Acknowledgment

The author is grateful to Sam Beckwith for his invaluable research.

Endnotes

- Typically loans under $100,000 to businesses and under $10,000 to individuals.

- Total commercial and industrial small business loans of $1 million or less to U.S. addresses, according to the FDIC Statistics on Depository Institutions.

- Credit card loans made by all depository institutions.

- See https://www.lendingclub.com/info/demand-and-credit-profile.action and http://www.prosper.com/Downloads/Legal/Prosper_Prospectus_2013-09-06.pdf.

- The Utah Department of Financial Institutions is a major regulator of platforms that use WebBank to originate loans.

- Fumiko Hayashi and Joanna Stavins, "Effects of Credit Scores on Consumer Payment Choice" (Federal Reserve Bank of Boston public policy discussion paper no. 12-1, 2012), http://www.bostonfed.org/-/media/Documents/cb/PDF/ppdp1201.pdf.

- Large, diversified portfolios tend to have high yields. So far no Lending Club investor who has purchased 800 or more notes has suffered a loss, and more than 94 percent gain 6 percent to 18 percent or more. See http://www.lendingclub.com/public/diversification.action.

- White-label products are products that are manufactured by one company and sold by a company that puts its own brand and model number on the product.

- See https://www.lendingclub.com/public/lending-club-press-2013-06-20.action.

Articles may be reprinted if Communities & Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

Richard D. Olson Jr., Randolph Savings Bank