September 2016: Top Challenges

Peter Davis/Federal Reserve Bank of Boston

December 2015: Perspectives on the affordability of housing, employment opportunities and the financial well-being of lower-income households

{kind=link}

About the Survey

The New England Community Outlook Survey is a compilation of service providers' perceptions of the economic and financial conditions of lower-income communities and individuals in New England and the organizations that serve them. Previous reports are available, and community leaders interested in becoming a part of these surveys may contact Kaili Mauricio or Anthony Poore.

In December 2015, the Federal Reserve Bank of Boston again conducted a semiannual New England Community Outlook Survey. As with previous iterations of the survey, service providers were asked about emerging issues facing lower-income communities, including questions about the financial well-being of their constituencies and the availability of affordable housing.

Access to affordable housing consistently arises as a topic of concern in the New England Community Outlook Survey. Specific survey questions address the current availability of affordable housing and its anticipated availability in the next six months. Service providers who responded to the December 2015 survey expect no change in the availability of affordable housing, highlighting that a lack of affordable housing is a persistent problem for New England's low-income individuals and families.

This report complements the survey respondents' commentary with a discussion of the demand for affordable housing and what is being done to address this concern.

Top Challenges Facing Lower-Income Communities

The top three challenges facing lower-income communities, as ranked by the respondents in this iteration of the New England Community Outlook Survey, are access to affordable housing, the availability of employment opportunities, and state and local budget cuts (Figure 1). Access to affordable housing shifts into the top spot, overtaking employment opportunities, which falls to second. Forty-two percent of survey respondents working outside the housing sector rank the lack of affordable housing as a top challenge.

{kind=link}

Figure 1

Peter Davis/Federal Reserve Bank of Boston

Affordable Housing: The Plight of Low-Income Individuals

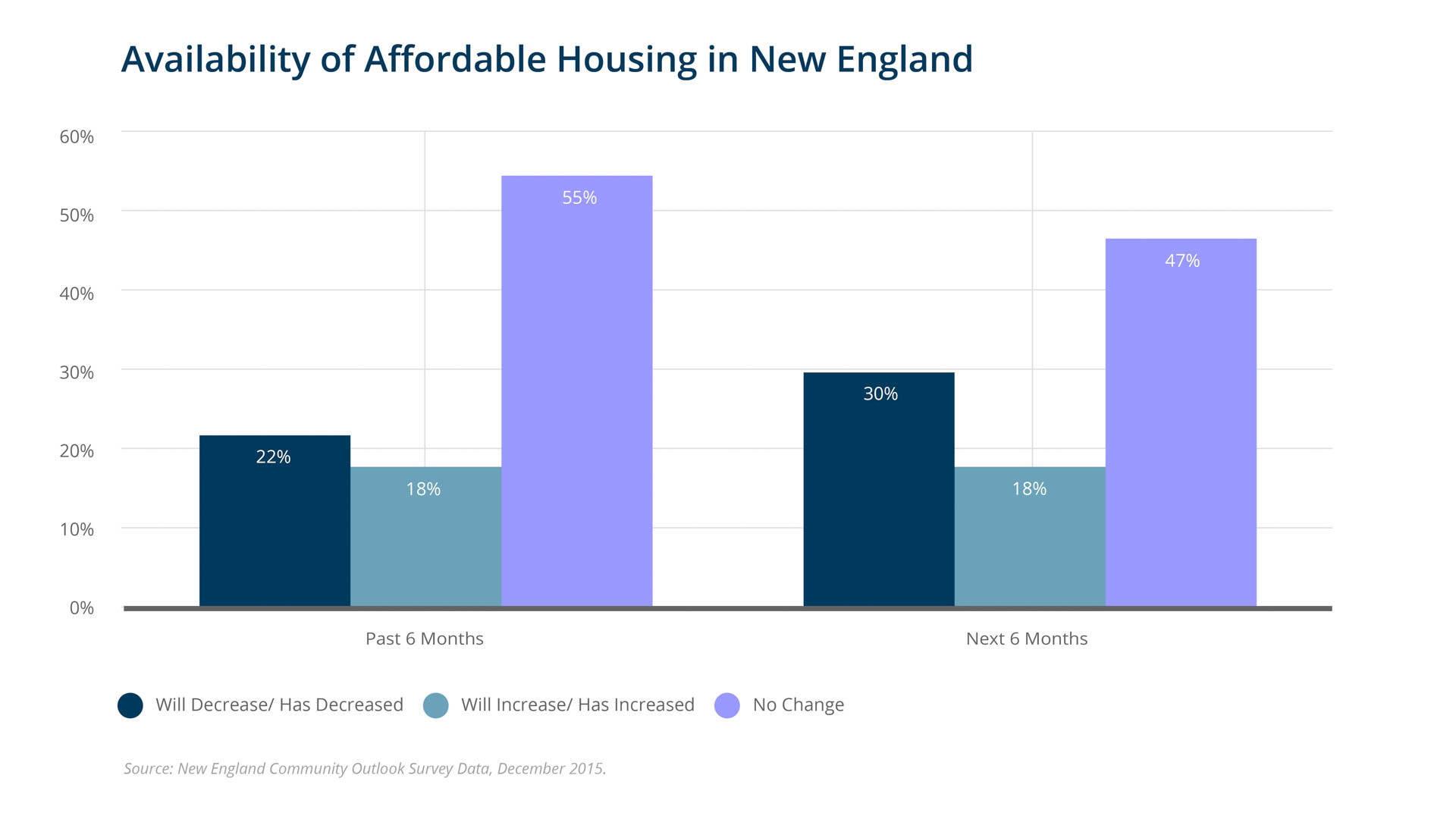

According to survey responses throughout New England, affordable housing units continue to be in short supply. The U.S. Department of Housing and Urban Development (HUD) defines affordable housing as "housing for which the occupant(s) is/are paying no more than 30 percent of his or her income for gross housing costs, including utilities."1 Since 2013, survey respondents have indicated a persistent shortage of affordable housing units. More than half of survey respondents cited no change in the availability of affordable housing in the past six months, but some expected an increase in availability within the next six months (Figure 2). Nonetheless, HUD predicts that the availability of affordable housing is likely to worsen in the coming years.2 In New England, 51 percent of renters and 33 percent of homeowners are cost-burdened3 (Figure 3). Access to affordable housing is most problematic for lower-income individuals. Although interest rates have declined, purchasing a home is out of reach for many lower-income families. Many families have insufficient cash for a down payment and closing costs, have preexisting debts, have low credit scores, and are subject to higher borrowing costs.4 Lack of wealth—specifically liquid financial wealth—limits households from becoming homeowners.5 To secure housing, many individuals are forced to rent, since they are unable to qualify for a mortgage. Renters who annually earn less than $50,000 are twice as likely to be cost-burdened than homeowners earning the same income. The National Low Income Housing Coalition reported that to obtain affordable housing renters would need a housing wage6 in excess of $16 per hour to rent a two-bedroom unit in New England, which is more than twice the Federal Minimum Wage and slightly more than what the "Fight For $15" movement is supporting. The housing wage in Massachusetts, the most costly New England state, would be $24.64, requiring an annual salary of approximately $51,000.7 In New England, 62 percent (nearly 2 million residents) who rent housing earn under $50,000, with more than two-thirds making less than $25,000 a year.8 The ongoing movement advocating an increase of the minimum wage to $15 could help to bridge the disparity between lower incomes and housing affordability.

Some respondents reported that policymakers either ignore or do not understand the need and associated demand for affordable housing, with one survey respondent from Rhode Island noting: "There is no significant state funding programs for affordable housing in Rhode Island.9 Another respondent stated that policymakers have "[an] unwillingness to address workforce housing using city assets." New England Community Outlook Survey respondents continued to witness firsthand that the lack of affordable housing extends throughout New England.

{kind=link}

Figure 2

Peter Davis/Federal Reserve Bank of Boston

{kind=link}

Figure 3

Peter Davis/Federal Reserve Bank of Boston

Job Opportunities

Although over half of respondents report that they expect job availability to increase during the next year, one-third of respondents report that they expect no change in job availability in their communities. Survey respondents shared a common concern about the lack of workforce-development training opportunities. For example, a survey respondent working in the economic-development field working in western Massachusetts stated: “We have a lot of jobs but [lack] a workforce that is trained or educated enough to take the available jobs. Employers are concerned that if they provide training to the employee, the employee will be hired by another firm, wasting the employers’ investment.10 Instead, the expectation is that employees should come to the job with the necessary prerequisite skills, which is not always feasible.”

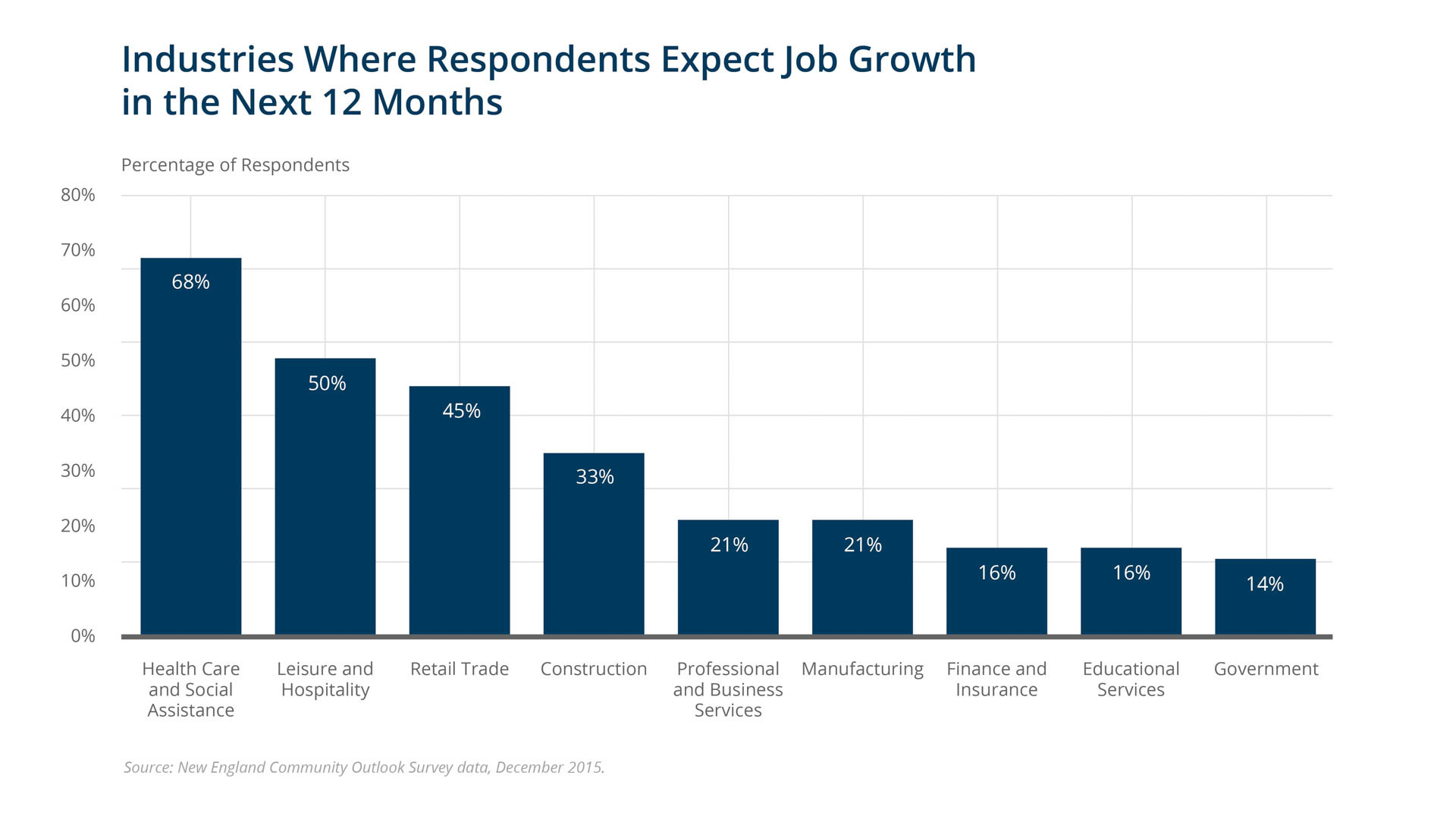

Respondents were asked to rank the top industries in which they expected job opportunities would occur during the next year. Sixty-nine percent of all respondents expected jobs in the healthcare and social-service sectors to increase in the upcoming year, whereas only over half of the respondents in Maine and New Hampshire felt that job opportunities in these sectors would increase in the forthcoming year. Perception of a possible increase in these types of jobs may be attributed to members of each state’s aging population leaving the workforce, coupled with an increased demand for healthcare services. The US Bureau of Statistics predicted healthcare occupations and related industries will have the fastest growth in employment opportunities and will add the most jobs between 2014 and 2024. Greater numbers of workers in the region’s labor force will be reaching retirement age and creating job vacancies.11 As reported in the survey, opportunities in the leisure and hospitality industries are expected to grow significantly in New Hampshire as compared to other states in New England. Only 14 percent of survey respondents expect government sector jobs will experience growth over the next year.

{kind=link}

Figure 4

Peter Davis/Federal Reserve Bank of Boston

Financial Well-Being

Respondents were asked about the financial well-being of their constituencies. For the purpose of this survey, "financial well-being" is defined as the ability to fund basic needs, to stay current on debt service, and to save and invest for the future. Almost half report no change in the past six months nor do they expect any changes among their constituencies in the upcoming six months (Figure 4). Past Community Outlook Surveys also have reported this trend.

{kind=link}

Figure 5

Peter Davis/Federal Reserve Bank of Boston

Demand for Services

Survey respondents continue to report an increase in the demand for their services, and they expect future increases in demand (Figure 5).

{kind=link}

Figure 6

Peter Davis/Federal Reserve Bank of Boston

Methodology

Since 2010, the Federal Reserve Bank of Boston has conducted the New England Community Outlook Survey. The respondents represent organizations providing direct services to lower-income households. Organizations are asked twice a year to designate a senior staff member to respond to the short survey. For the latest iteration of the survey, 99 service providers from the economic development, affordable housing, community action, human services, and workforce development sectors in each of the six New England states responded to 15 multiple-choice and fill-in questions. We asked respondents to comment on the changes in conditions over the previous six months and to project changes over the next six months. Respondents completed the survey in December 2015.

Data collected represent the opinions of service providers who completed the survey. While we strive to include a reasonably representative sample in our survey, responses should not be interpreted to represent the opinions of all service providers in New England.

About the Authors

About the Authors

Anjali Sakaria

Endnotes

- US Department of Housing and Urban Development, HUD Glossary. https://www.huduser.gov/portal/glossary/glossary_a.html

- US Department of Housing and Urban Development, HUD at 50: Creating Pathways to Opportunity (Washington, DC: GPO, October 2015). https://www.huduser.gov/portal/publications/pdf/HUD-at-50-creating-pathways-to-Opportunity.pdf

- "Cost-burdened" is defined by the US Department of Housing and Urban Development as households spending 30 percent or more of their income on housing.

- US Department of Housing and Urban Development, "Paths to Homeownership for Low-Income and Minority Households," Evidence Matters (2012). https://www.huduser.gov/portal/periodicals/em/fall12/highlight1.html

- Christopher E. Herbert and Winnie Tsen, "The Potential of Down Payment Assistance for Increasing Homeownership Among Minority and Low-Income Households," Cityscape 9, no. 2 (2007): 153-83.

- "Housing wage" is defined by the US Department of Housing and Urban Development (HUD) as the estimated full-time hourly wage a household must earn to afford a decent rental unit at HUD-estimated Fair Market Rent while spending no more than 30 percent of its income on housing costs.

- National Low Income Housing Coalition, Out of Reach 2015 (Washington, DC: NLIHC), 11, 14. http://nlihc.org/sites/default/files/oor/OOR_2015_FULL.pdf

- Author's calculation using US Census Bureau 2014 American Community Survey 1-Year Estimates, Table S2503 (Washington, DC: US Census Bureau, 2014).

- In 2014, Rhode Island allocated approximately 11.8 million towards affordable housing, but funding decreased in 2015 due to the final allocations of the Building Home Rhode Island program. Source: Consolidated Annual Performance & Evaluation Report. Program Year 2014. State of Rhode Island. 4. http://www.rhodeislandhousing.org/filelibrary/CAPER_2014_FinalDraft.pdf and HousingWorks RI at Roger Williams University. Projecting Future Housing Needs Report. (Rhode Island), 36. http://www.rhodeislandhousing.org/filelibrary/HWRI-Projecting-Future-Housing-Needs-Report-04-06-16.pdf

- Peter Cappelli, "Why Companies Aren't Getting the Employees They Need," Wall Street Journal, October 24, 2011.

- Bureau of Labor Statistics.Employment Projections: 2014-24 Summary (Washington, DC: US Department of Labor, December 8, 2015). http://www.bls.gov/news.release/ecopro.nr0.htm