Are Recently Issued Credit Card Accounts More Risky?

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

In a recent Consumer Financial Protection Bureau (CFPB) study of credit card delinquency rates (Fulford and Gibbs 2024), the authors find that credit card accounts opened in 2021, 2022, and 2023 that became delinquent—payments 30 days past due—did so faster than accounts opened in 2019, before the COVID-19 pandemic. They attribute this outcome to banks issuing credit cards to riskier consumers in the more recent years, that is, consumers who were less likely to pay off their debts.

I use Federal Reserve Y-14M data on the majority of credit card accounts issued by US banks1 to test the authors’ results and conclusions. I find evidence that credit card accounts opened in 2022 and 2023 that became delinquent entered delinquency faster than accounts opened in 2018 and 2019, but this change appears to have been only temporary. The most recent data, from 2024, indicate that the age of newly delinquent accounts—the elapsed time between an account’s opening and its entering delinquency—has reverted to the long-term trend in which the age remained relatively constant over time.

Sign up for Research Department Updates.

I also find evidence that new accounts opened during the COVID-19 period in 2021 and 2022 were issued to consumers with lower credit scores compared with accounts opened shortly before the pandemic. Lower credit scores could indicate that those account holders had a higher risk of defaulting on their loans. However, that trend also has reversed, as the average credit score of new account holders increased starting in 2022, and at the end of 2024, it was higher than the pre-COVID-19 level. The findings suggest that any erosion of lending standards that took place during the early stages of the pandemic has been reversed. Rising delinquency rates can contribute to a weakening of the economy, so a reversal of relaxed lending standards provides some assurance that economic conditions are not deteriorating.

My findings are consistent with results from the Federal Reserve Board’s quarterly Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS).2 The SLOOS shows that during the pandemic—in 2020, 2021, and in the first quarter of 2022—banks reported that they had eased standards for credit card loans. In other words, they lowered the minimum credit scores required for approval of credit card applications. Banks reported that they did not change standards during the second quarter of 2022. They then tightened standards in the third quarter of that year and in every subsequent quarter through 2024:Q4, which is covered by the most recent available SLOOS survey (from January 2025).

The main reason why my findings differ somewhat from those of Fulford and Gibbs (2024) is that their data end in early 2024, whereas I use data through December 2024. Both studies find that banks loosened their lending standards during the pandemic, but the most recent data suggest that lending standards, like the average age of newly delinquent credit card accounts, have returned to their long-term, relatively constant level.

Additionally, Fulford and Gibbs (2024) use the CFPB’s Consumer Credit Information Panel (CCIP) data, which are provided by credit bureaus, whereas the Y-14M data that I use in this study were provided directly by the lenders and include the majority of US credit card accounts. There are some differences between the samples. For example, the Y-14M banks are instructed to keep accounts on their books for only 12 months after they are closed (banks usually close an account after a payment is severely past due, but the exact timing varies by lender). By contrast, closed accounts remain in the CCIP data and therefore can be tracked for a longer period after becoming delinquent.

Delinquency Rate Increased Starting in 2021 but Appears to Have Leveled Off

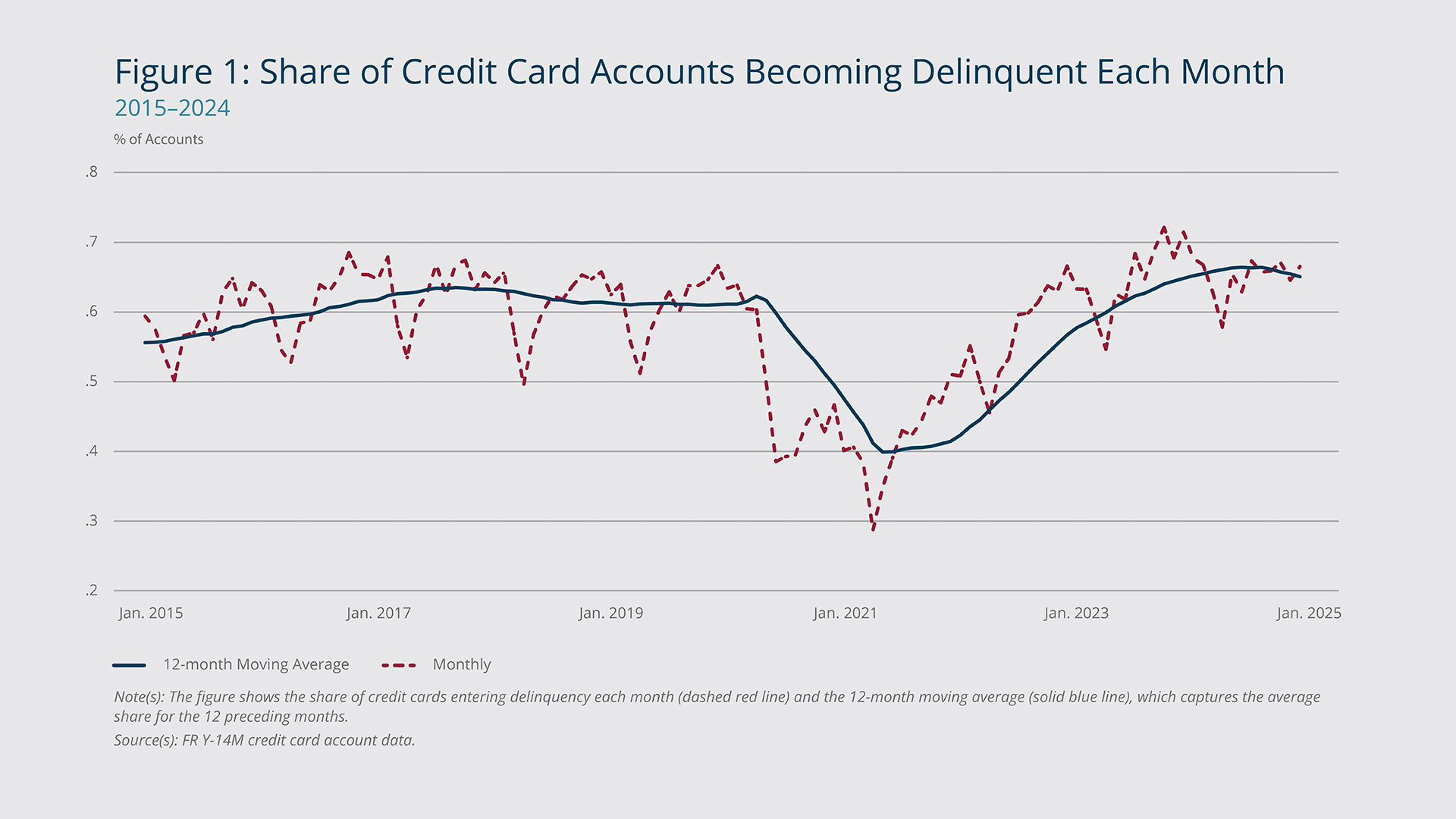

At the start of the COVID-19 pandemic, in 2020, a combination of pandemic transfers (specifically payments from the Coronavirus Aid, Relief, and Economic Stimulus [CARES] Act) and limited spending opportunities (due to shutdowns and other factors) helped reduce credit card borrowing in the United States. Following a relatively steady long-term trend, the share of credit card accounts that became delinquent in a given month declined rapidly as consumers paid back large portions of their credit card debt. However, the delinquency rate began rising again in May 2021.

{kind=link}

Federal Reserve Bank of Boston

Figure 1 shows the share of credit card accounts becoming delinquent each month (dashed red line), which is subject to substantial seasonal and monthly volatility, and the 12-month moving average (solid blue line), which captures the average growth for the 12 preceding months. The delinquency rate increased steeply in 2022 and 2023, but the pace of that growth slowed substantially in 2024, and the rate actually declined at the end of 2024. The most recent data suggest that the delinquency rate may plateau at a level similar to its pre-COVID-19 long-term trend.

Cardholders with the Lowest Credit Scores Have Been Most Likely to Hold Delinquent Accounts

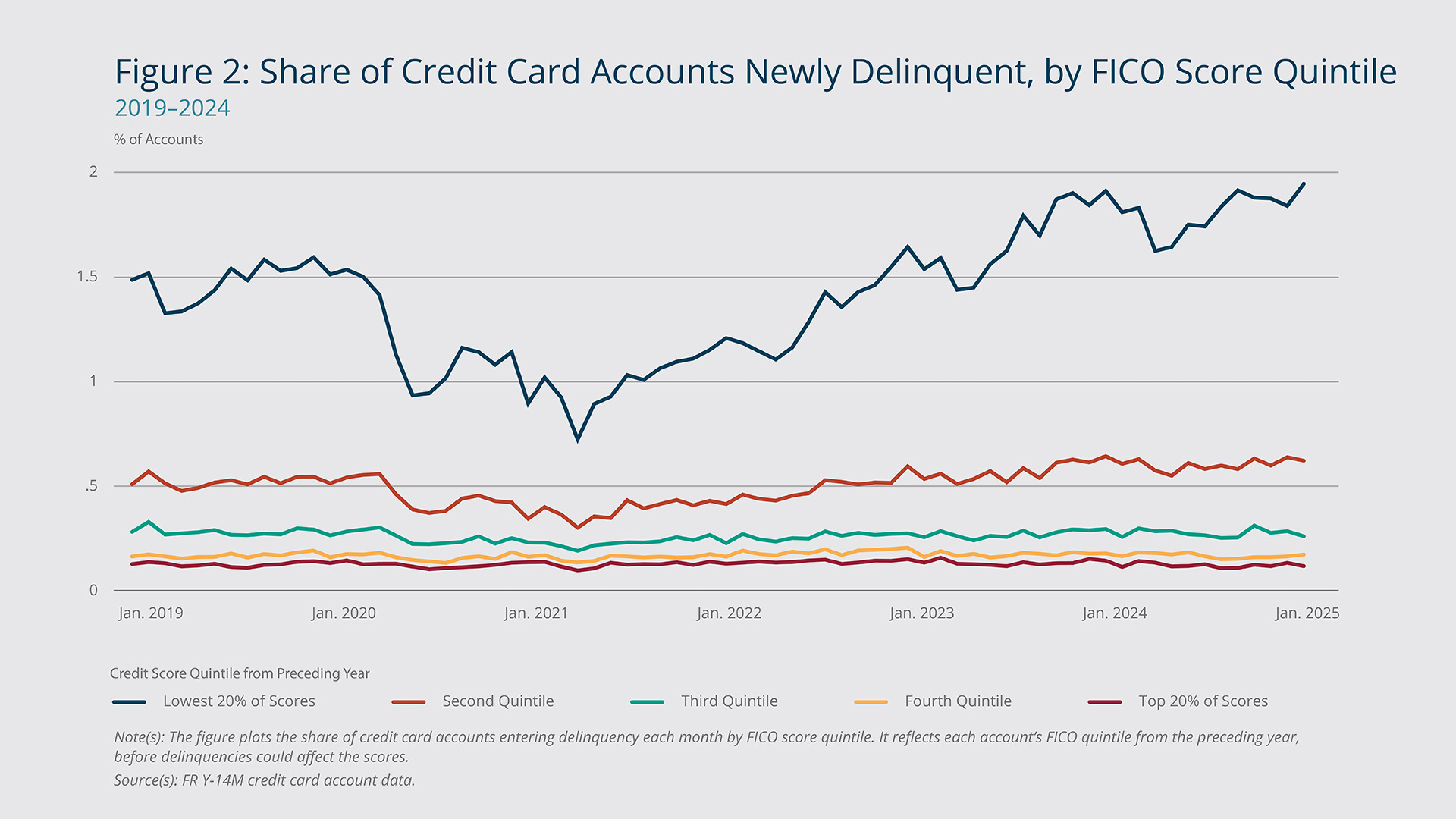

As Figure 2 shows, and Driscoll et al. (2024) find, consumers in the bottom credit-rating quintile drove the increase in the delinquency rate during the 2022–2023 period. The Y-14M data include each account holder’s credit rating as measured by their FICO score.3 The findings depicted in Figure 2 reflect each account’s FICO quintile from the preceding year, before delinquencies could affect the scores. The share of accounts in the bottom FICO quintile that became delinquent increased from 0.73 percent in April 2021 to a peak of 1.95 percent in December 2024, even as the overall delinquency rate declined at the end of last year. Because accounts of cardholders with lower credit scores are more likely to become delinquent, issuing new cards to lower-score consumers could lead to higher delinquency rates.

{kind=link}

Federal Reserve Bank of Boston

Comparing the share of accounts entering delinquency by income cohort shows that consumers with an annual household income of less than $50,000 had higher delinquency rates than consumers in higher-income cohorts, both before the pandemic (from 2015 through 2019), when delinquency rates were relatively steady, and from 2020 through 2024, when delinquency rates changed substantially—decreasing sharply, rising, and decreasing again. While the share of accounts entering delinquency rose more steeply for lower-income consumers than for higher-income consumers, it increased for all income groups from 2021 through 2023 (Appendix Figure A1).

Average Age of Newly Delinquent Accounts Is Now Close to the Long-term Level

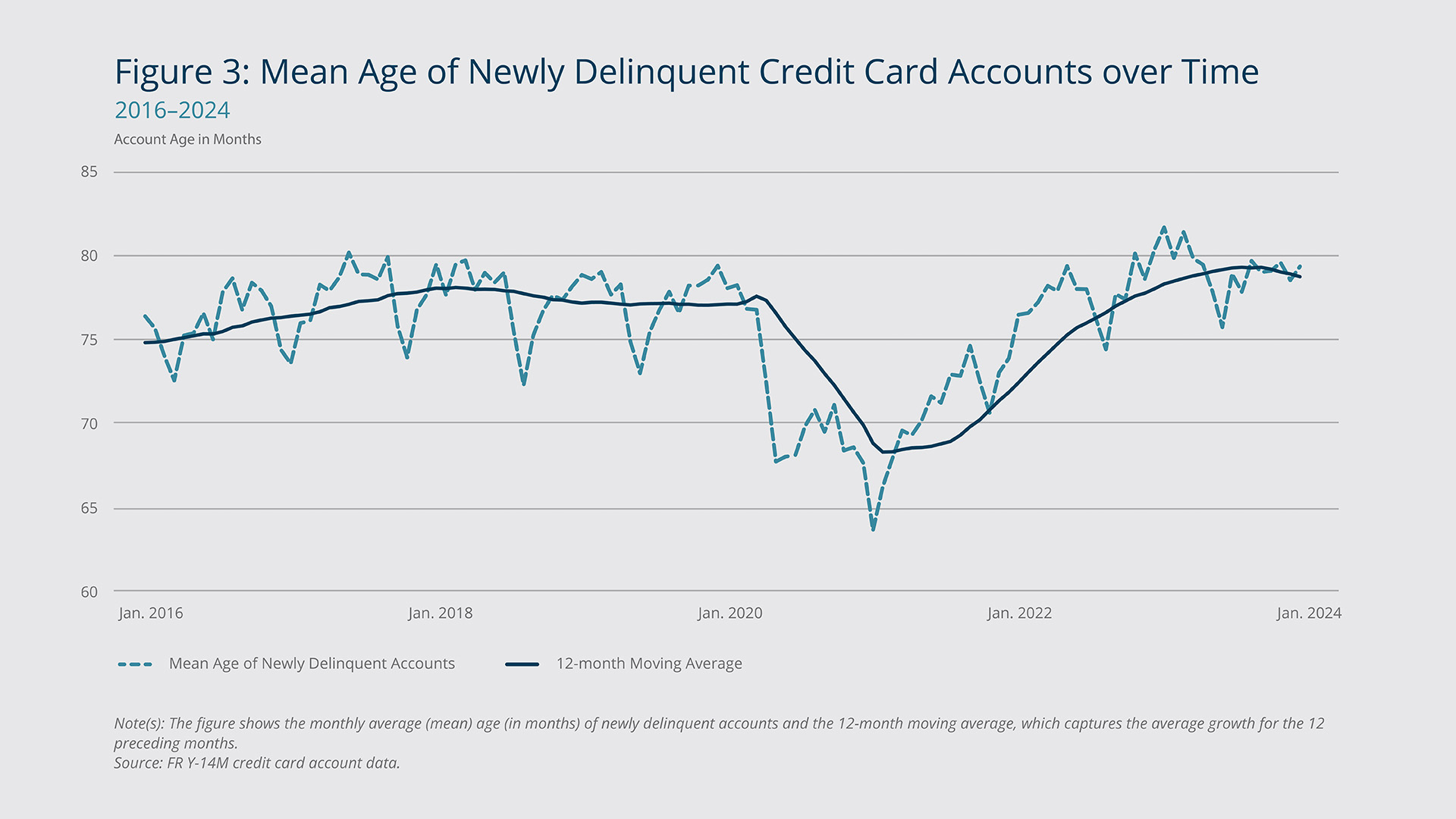

Because the mean age of newly delinquent accounts exhibits substantial month-to-month volatility, it is more useful to look at longer-term changes. The solid line in Figure 3 plots the 12-month moving average of the mean age—each plot point in the figure depicts the average mean age for the 12 preceding months. When delinquency rates decreased in 2020 and early 2021, the mean age when accounts became delinquent rose: The 12-month moving average increased from 69 months before the start of the pandemic in early 2020 to 79 months at its peak in mid-2021. (The monthly mean peak, depicted by the dashed line, was 83 months in April 2021.) I find evidence that the mean age of newly delinquent accounts declined in the second half of 2021 and in 2022, but even at its trough, in 2023, the mean age was on par with the longer-term mean observed before the pandemic.

{kind=link}

Federal Reserve Bank of Boston

Moreover, I find that the median age of newly delinquent accounts in 2023 was the same as the median age right before the start of the pandemic, in February 2020. Similarly to the mean age, the median age increased during the early stages of the pandemic, when the delinquency rate dropped, then declined in 2021 and 2022. Thus, the data indicate that the changes in the age of newly delinquent accounts that took place during the pandemic were temporary.

Average Age of Delinquency Varies across Account Vintages

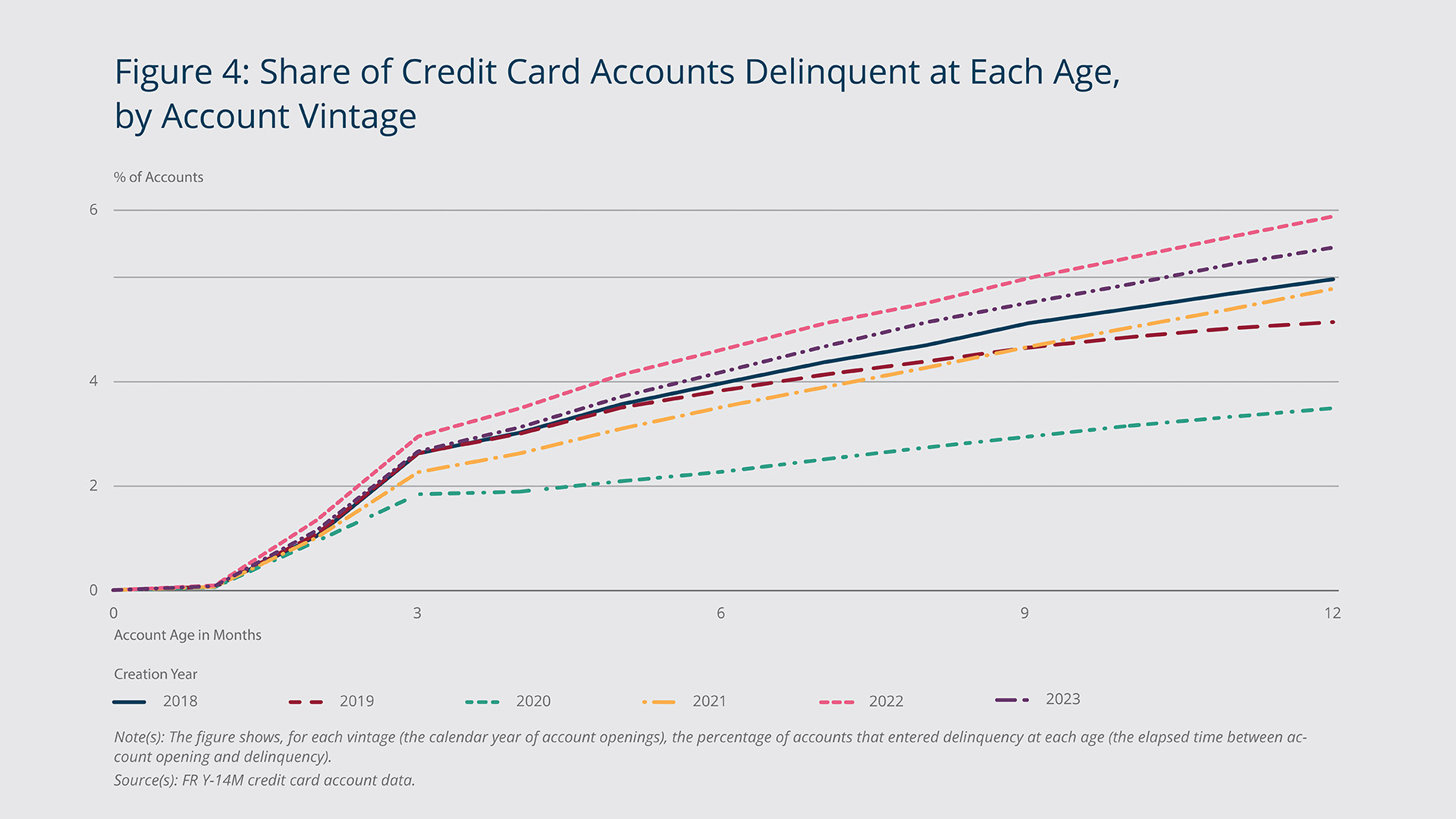

When I test whether a given credit card account’s vintage—the calendar year when it was issued—affected the age at which it became delinquent, I find, not surprisingly, that accounts opened in 2020 (the first year of the pandemic) were the sample’s least likely to become delinquent within 12 months of being issued; less than 3 percent became delinquent in the year following origination. Accounts opened in 2019 had the sample’s second-lowest rate at just over 4 percent. By contrast, nearly 6 percent of accounts created in 2022 became delinquent in their first year (Figure 4).4

{kind=link}

Federal Reserve Bank of Boston

As Figure 4 shows, accounts created in 2022 and 2023 were the most likely to be delinquent 12 months after origination relative to accounts opened in other years of the sample. The differences across account vintages are fairly small at 12 months after origination. They may grow larger, but as noted earlier, Y-14 banks are instructed to continue reporting data on an account for only 12 months after it is closed. Therefore, our findings are relevant for only the first year of an account’s delinquency, and we cannot reject the hypothesis that differences across vintages expand as the accounts age.

There was no notable difference across vintages in the average balance on newly delinquent accounts, except for accounts opened during the early part of the pandemic, in 2020 and 2021. The average balance on newly delinquent accounts from that vintage was lower compared with the other vintages, which is consistent with the average balance on all credit card accounts being lower during that period.

Banks Opened Riskier Accounts for Only a Brief Period

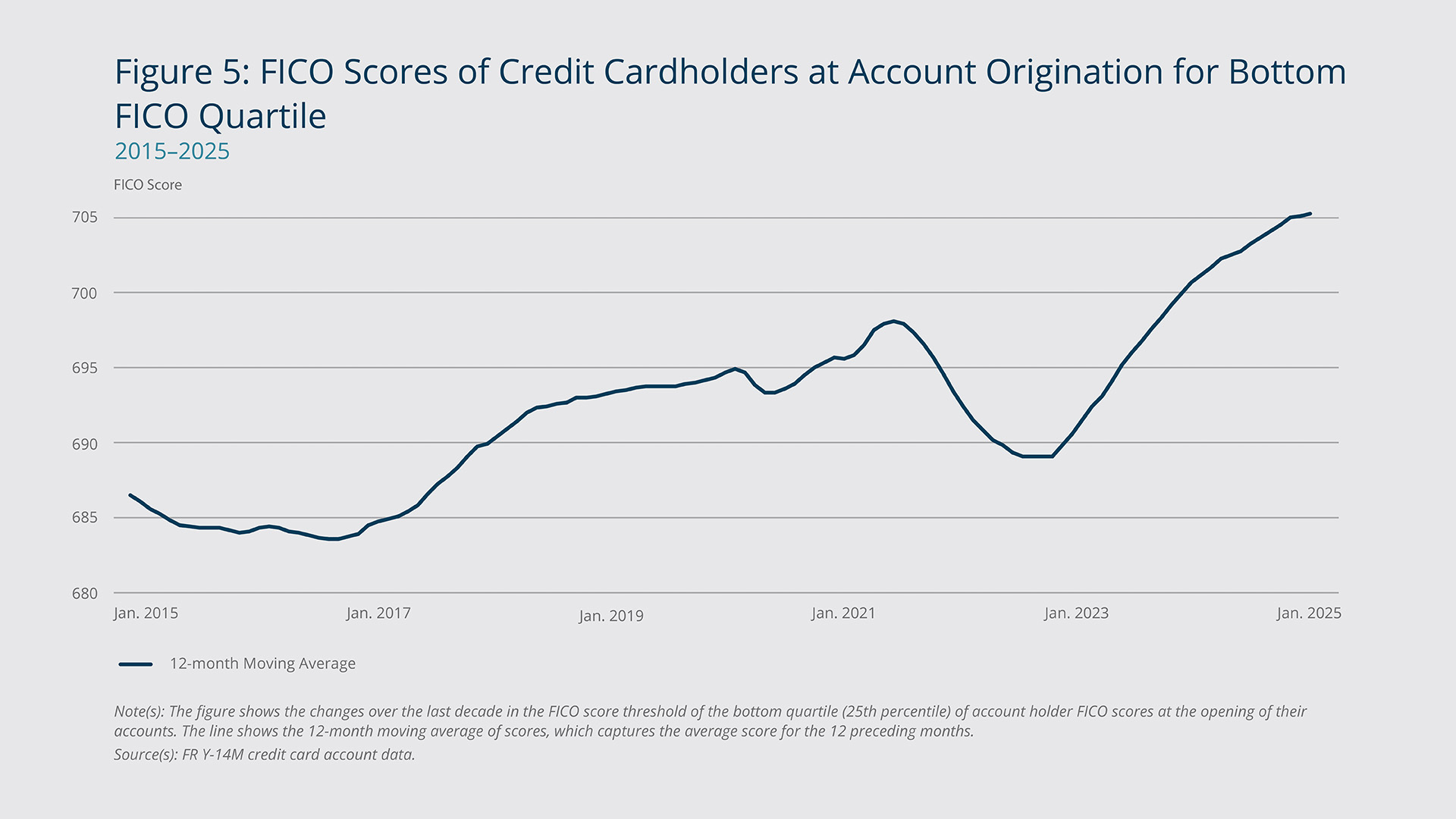

I find evidence that, on average, consumers who were issued credit cards from banks in 2022 and 2023 had a higher risk of default compared with consumers issued credit cards in the pre-pandemic period of 2018 and 2019. Figure 5 plots the threshold of the bottom quartile (25th percentile) of account holder FICO scores at the origination of their accounts. The higher the 25th percentile score, the lower the default risk of the accounts in the quartile.

{kind=link}

Federal Reserve Bank of Boston

As the chart shows, the percentile demarcating the bottom FICO quartile for new accounts has gradually risen over the past decade. (Month-to-month volatility has been substantial, so the chart shows a smoother, 12-month moving average of credit scores.) This trend reversed in 2021 and 2022, but the bottom percentile started rising again in November 2022 and exceeded its previous peak in October 2023. While some of the increase in the observed credit scores might have been driven by pandemic-era shifts in the credit score distribution (Driscoll et al. 2024), that upward “credit score migration” primarily took place from 2020 to 2022, before the increase in FICO scores of new account holders.

Plotting other percentiles, such as the 10th or the median, yields a similar picture—albeit at different baseline levels—of a decline in 2021 and 2022 that has since been reversed. These findings serve as another piece of evidence indicating that the changes in the riskiness of new accounts that took place early in the pandemic might have been only temporary.

The Age When Accounts Became Delinquent Varied by Cardholder Income

For each credit card account, I look at the account holder’s income at the time the account was created5 and find substantial differences in the rate of growth in the number of accounts held by each income cohort. As Appendix Figure A2 shows, when income is adjusted for inflation, the total number of credit card accounts increased after January 2020 for every income cohort, but the number of accounts held by the bottom income cohort—households with an annual income of less than $25,000—increased less than the number of accounts held by any other income cohorts. While the number of accounts held by bottom-income households increased 7 percent from January 2020 to December 2024, the number of accounts for most of the other income groups rose more than 20 percent.

When I base the analysis on account holders’ nominal income and do not adjust for inflation, I find that the number of accounts held by consumers with household income of less than $25,000 dropped 8.4 percent, because inflation reduced the share of account holders in that income group. But even after adjusting for the effects of inflation, the analysis shows that the share of accounts held by the bottom-income group of consumers has declined over time, while the share held by higher-income consumers has increased.

Calculating the percentage change in the median age of newly delinquent accounts from January 2020 to December 2024 by income cohort (Appendix Figure A3) shows that for all income cohorts, the median age increased during the early part of the pandemic, when delinquency rates dropped. (Income is measured at account opening and is adjusted for inflation; all income is in 2015 dollars.) Starting in mid-2021, delinquency rates increased, and the median age of newly delinquent accounts gradually declined again for all income cohorts.

Although the exact trajectory varied across income cohorts, the median age of newly delinquent accounts started rising again in 2023 or 2024 for all income cohorts, essentially reversing the earlier declines. The most recent data provide no evidence that credit card accounts are becoming delinquent more quickly after opening than they did before the pandemic. For each income cohort, the accounts that become delinquent now are, on average (median), older than the accounts that entered delinquency in the period before the pandemic.

Endnotes

- Each month, the Federal Reserve Board collects what are known as FR Y-14M data from bank holding companies (BHCs) with total consolidated assets of $100 billion or more. The data include detailed information on all the credit card accounts that the BHCs have on file. The accounts reported in the FR Y-14M data represent about three-quarters of the total bank credit card balances in the United States.

- Every quarter, the Federal Reserve Board conducts a survey of bank loan officers, the Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS). The reporting panel consists of 80 large US commercial banks, which provide qualitative information about their lending practices, including the provision of credit card loans to US consumers. See https://www.federalreserve.gov/data/sloos.htm.

- Lenders use FICO scores to assess a person’s creditworthiness and determine whether they should be extended credit. FICO scores range from 300 to 850, with higher scores indicating a greater likelihood of repaying debts on time.

- Note that the figure shows the share of all accounts issued in a given year that were delinquent at a particular age. Due to differences in how long banks allow delinquent accounts to remain open, other figures focus on the rate at which accounts enter delinquency instead of the stock of delinquent accounts. However, because Y-14M banks are instructed to continue reporting positive balances for 12 months after an account closes, this attrition poses less of an obstacle when the analysis is limited to the first year of an account’s existence.

- Although the Y-14M banks are required to report an account holder’s income every month starting from the time the account is issued, updated income is not reliably available.

References

Driscoll, John C., Jessica N. Flagg, Bradley Katcher, and Kamila Sommer. 2024. “The Effects of Credit Score Migration on Subprime Auto Loan and Credit Card Delinquencies.” FEDS Notes. Board of Governors of the Federal Reserve System. January 12.

Fulford, Scott, and Christa Gibbs. 2024. “Credit Card Delinquencies Are Higher than in 2019 Because Lenders Took on More Risk.” Consumer Financial Protection Bureau Blog. August 6.

About the Authors

About the Authors

Joanna Stavins,

Federal Reserve Bank of Boston

Joanna Stavins is a principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Email: Joanna.Stavins@bos.frb.org

Acknowledgments

The author thanks Julian Perry for providing excellent research assistance.

Resources

Site Topics

Keywords

- credit cards ,

- delinquency rates ,

- credit scores

JEL Codes

- G21 ,

- G51 ,

- D14 ,

- E42

Citation

Stavins, Joanna, “Are Recently Issued Credit Card Accounts More Risky?” 2025. Federal Reserve Bank of Boston Current Policy Perspectives No. 25-6.

Related Content

Do Consumers Rely More Heavily on Credit Cards While Unemployed?

Income and the CARD Act’s Ability-to-pay Rule in the US Credit Card Market

Job Loss, Credit Card Loans, and the College-persistence Decision of US Working Students

Credit Card Debt Puzzle: Liquid Assets to Pay Bills