How Firms’ Perceptions of Geopolitical Risk Affect Investment

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Geopolitical risk has intensified in recent years, driven by events such as Russia’s invasion of Ukraine, escalating tensions between the United States and China, and conflicts in the Middle East.1 But how risky is the geopolitical landscape according to US firms?

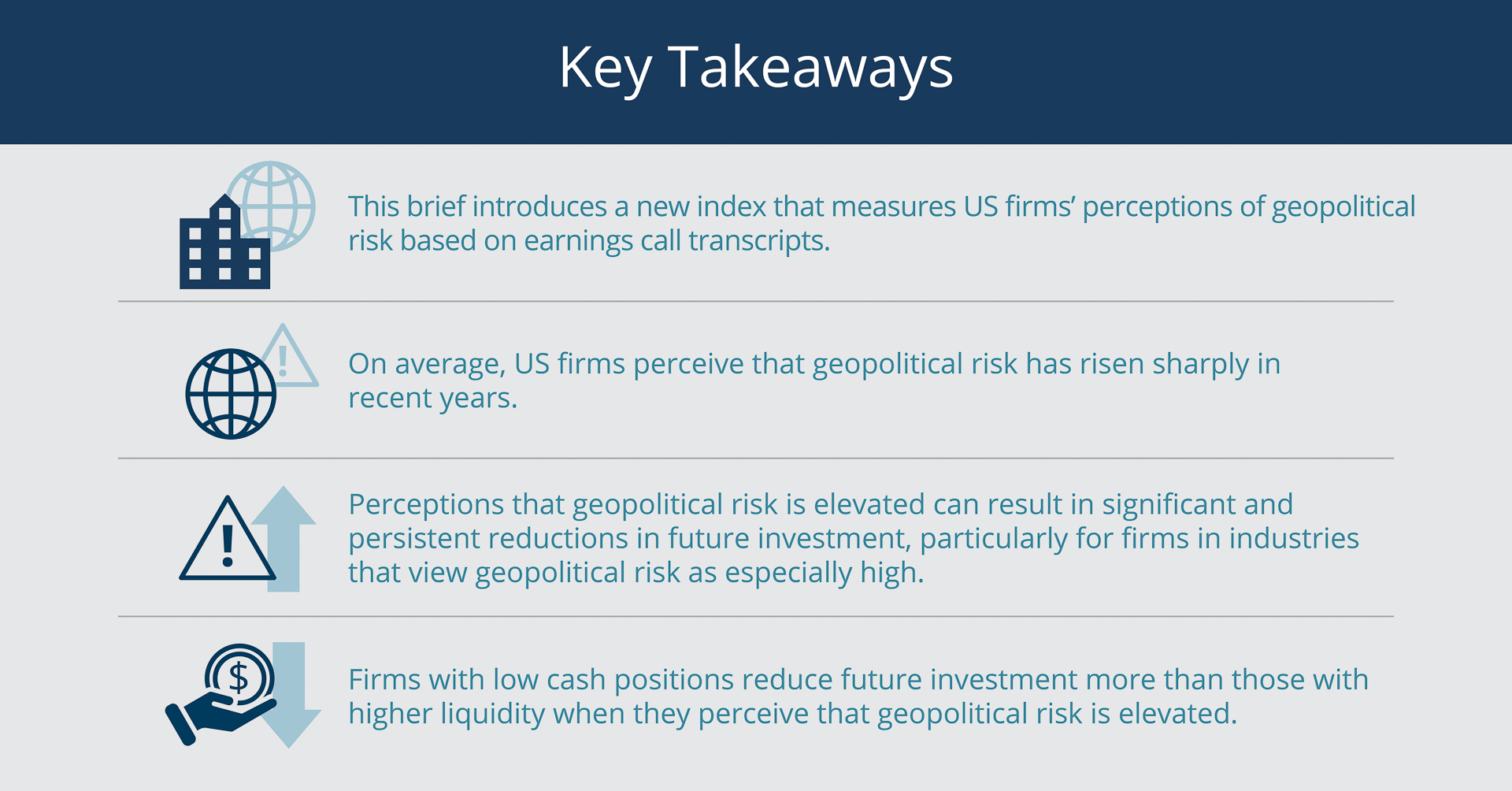

This brief presents a new index based on earnings call transcripts that reflects US firms’ perceptions of geopolitical risk and examines how those assessments affect their future investment, that is, their spending on long-term assets such as facilities, equipment, and technology.

Sign up for Research Department Updates.

I show that firms, on average, perceive that geopolitical risk has risen sharply in recent years, and that perceptions that risk is heightened can result in significant and persistent reductions in future investment, particularly for firms in industries that view geopolitical risk as especially high. Moreover, I show that the effect of risk perception can depend on firms’ cash positions—the proportion of liquid assets in total assets: Firms with low cash positions reduce future investment more than those with higher liquidity when they perceive that geopolitical risk is elevated.

Firms Perceive that Geopolitical Risk Has Escalated

To capture US firms’ perceptions of geopolitical risk, I construct a time-varying, firm-level measure based on text analysis of quarterly earnings call transcripts of publicly listed US companies. This method builds on the natural-language-processing techniques and the NL Analytics platform developed by Hassan et al. (2019, 2023).2

I quantify the extent of a firm’s focus on geopolitical risk by computing the share of sentences in its conference call discussions containing words related to geopolitical threats and actions as well as synonyms for risk or uncertainty. I adapted my dictionary of geopolitical-related words from the one used by Caldara and Iacoviello (2022), whose geopolitical risk measure is based on the contents of newspaper articles and how frequently they include references to adverse geopolitical events and associated risks.

Appendix Table A.1 presents details about the dictionary, which is organized into eight categories. Each category comprises a search query for the co-occurrence of words or phrases from two different sets; the first set contains topic words (for example, “war,” “military,” “terrorism”), and the second contains “threat” words for five of the categories and “act” words for three of the categories.

The following excerpts from the earnings call discussions of two firms contain words or phrases that match the index’s criteria for geopolitical risk–related content and illustrate the type of information that the index captures:

- “We experienced a further deceleration in growth following the start of the Ukraine war due to the loss of revenue in Russia as well as a reduction in advertising demand, both within Europe and outside the region. We believe that war introduced further volatility into an already uncertain macroeconomic landscape for advertisers” (April 2022).

- “...[T]he holiday period strength was offset during the quarter by the slower consumer demand across all categories for everyday gifting occasions, reflecting growing consumer concerns with rapidly rising inflation and geopolitical unrest” (April 2023).

These examples suggest that firms with higher geopolitical risk index values are likely more exposed to and affected by geopolitical risk.

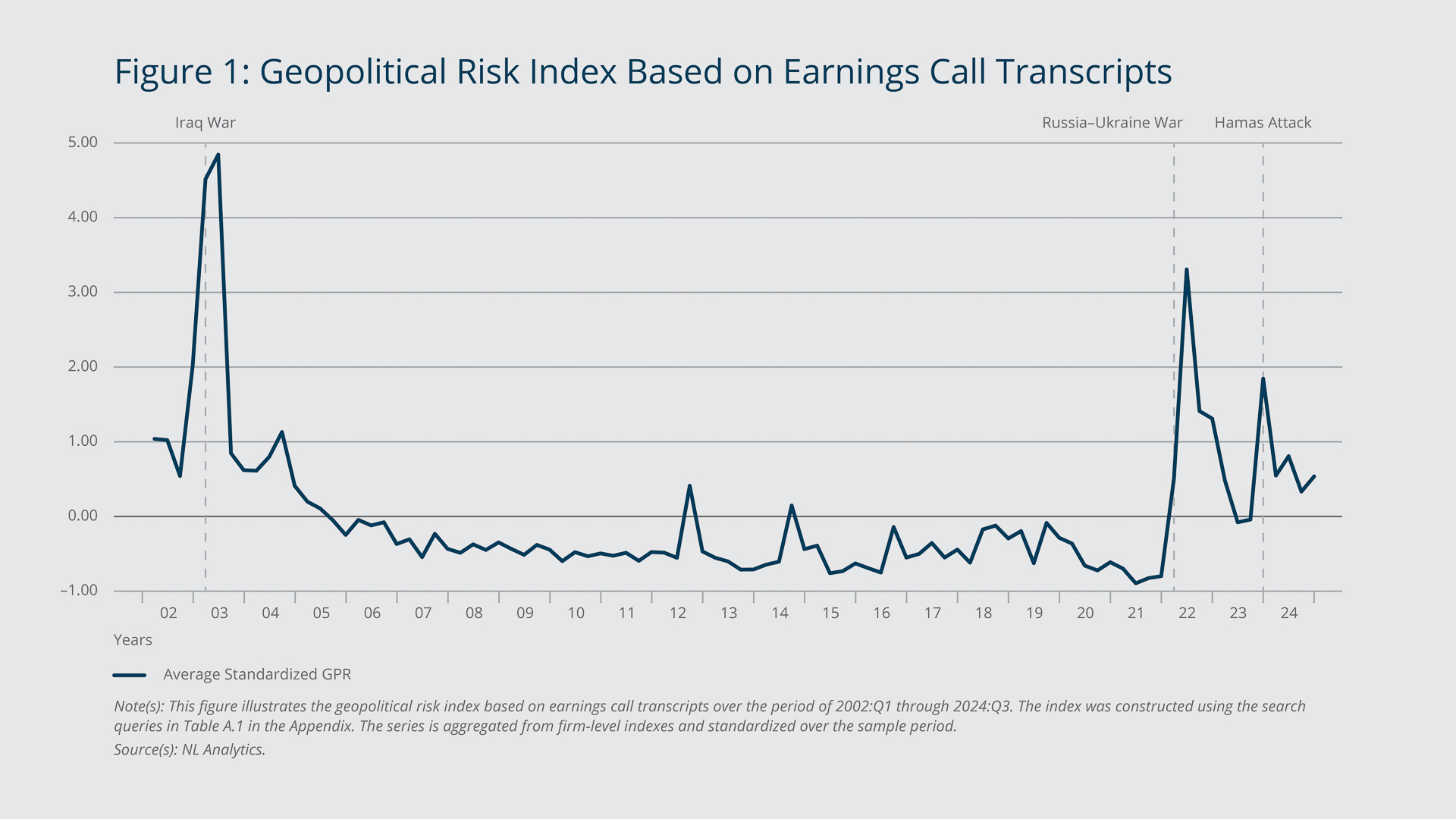

Figure 1 presents the geopolitical risk index, which reflects the average earnings call–derived risk-perception value across US firms, standardized over the sample period of 2002 through the third quarter of 2024.3 The figure shows US firms perceived that geopolitical risk was relatively subdued until recent years, when events such as the Russia–Ukraine war and conflicts in the Middle East drove sharp increases in the perceived risk. The index spiked to more than three standard deviations above the mean in 2022:Q2 and surged again in 2023:Q4.

{kind=link}

Federal Reserve Bank of Boston

This earnings call–based geopolitical risk index is highly correlated with the news story–based index developed by Caldara and Iacoviello (2022), exhibiting a correlation of 82 percent.

While the large spikes in the two indexes closely align, the earnings call–based index does not contain the smaller fluctuations observed in the news story–based index. The absence of these fluctuations indicates that firms’ perceptions of geopolitical risk are less influenced by moderate geopolitical events, likely because the firms are less directly affected by them.

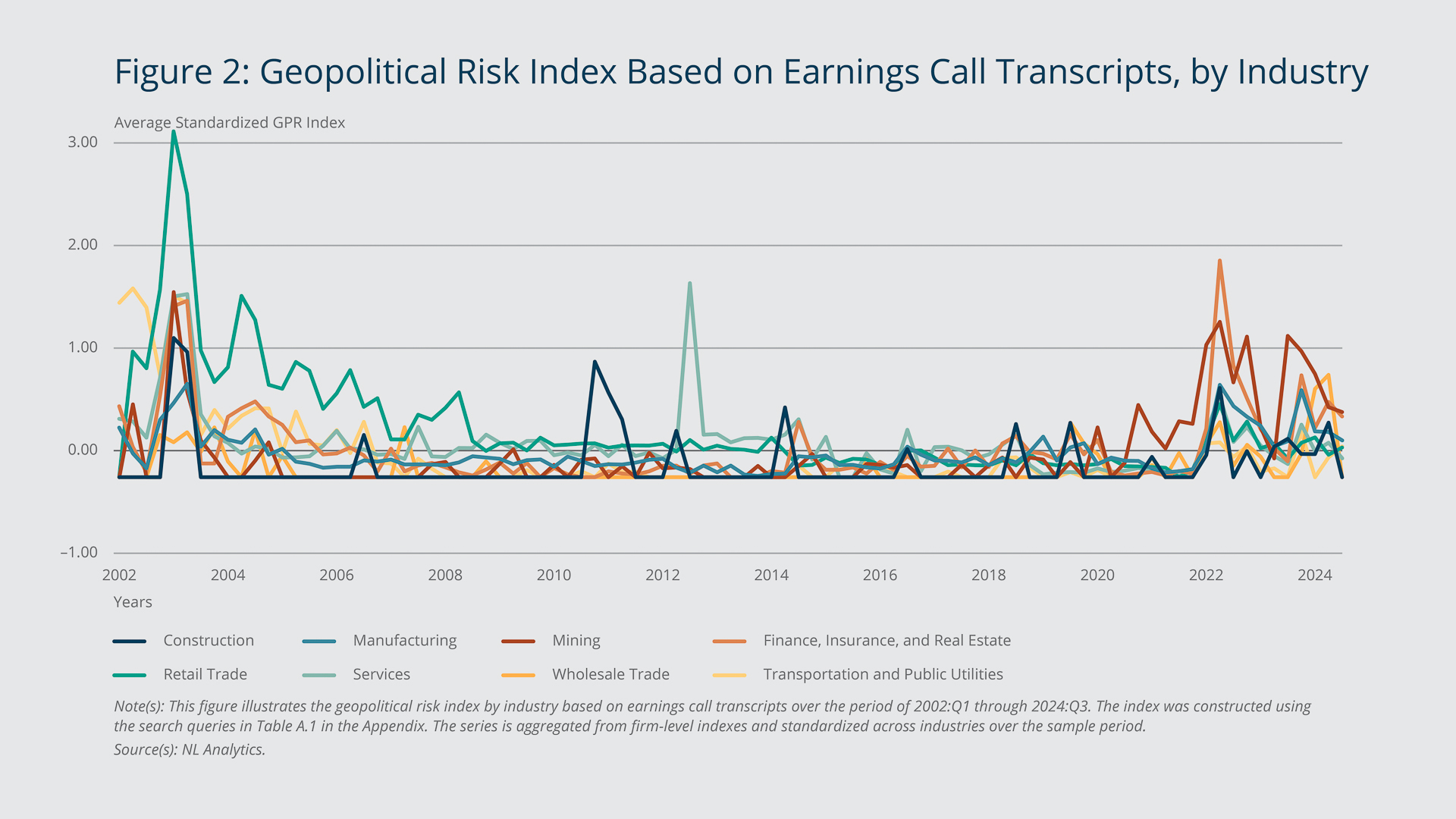

Figure 2 illustrates the earnings call–based geopolitical risk index across industries. The industries with the highest geopolitical risk index values are finance, mining (including oil extraction firms), and manufacturing; manufacturing firms tend to be involved in exporting and importing. Over the last few years, the risk index for these industries has stood approximately one to two standard deviations above the sample mean.

{kind=link}

Federal Reserve Bank of Boston

Perceptions that Geopolitical Risk Is Higher Result in Significant Reductions in Future Investment for US Firms in Affected Industries

Using the new index to estimate the impact of geopolitical risk on investment by US firms, I find that firms in industries that view geopolitical risk as being high significantly reduce future investment in response to perceptions that the risk is heightened. Additionally, in these industries, firms with low cash positions reduce future investment more significantly compared with higher-cash-position firms when they perceive an increase in geopolitical risk.

I conduct my analysis using lag-augmented local projections, a well-established method in the empirical macroeconomics literature (Jordà 2005; Montiel Olea and Plagborg-Moller 2021). In particular, I investigate potential heterogeneity across industries. I analyze whether firms in industries that perceive geopolitical risk as being high respond differently from firms in other industries to increases in the risk index. Industries are ranked quarterly based on their geopolitical risk index value and classified in quartiles or deciles of the distribution.

The estimation results show that while geopolitical risk does not significantly affect firms’ rates of investment on average, firms in industries perceiving that risk is high significantly reduce future investment in response to an increase in the geopolitical risk index.

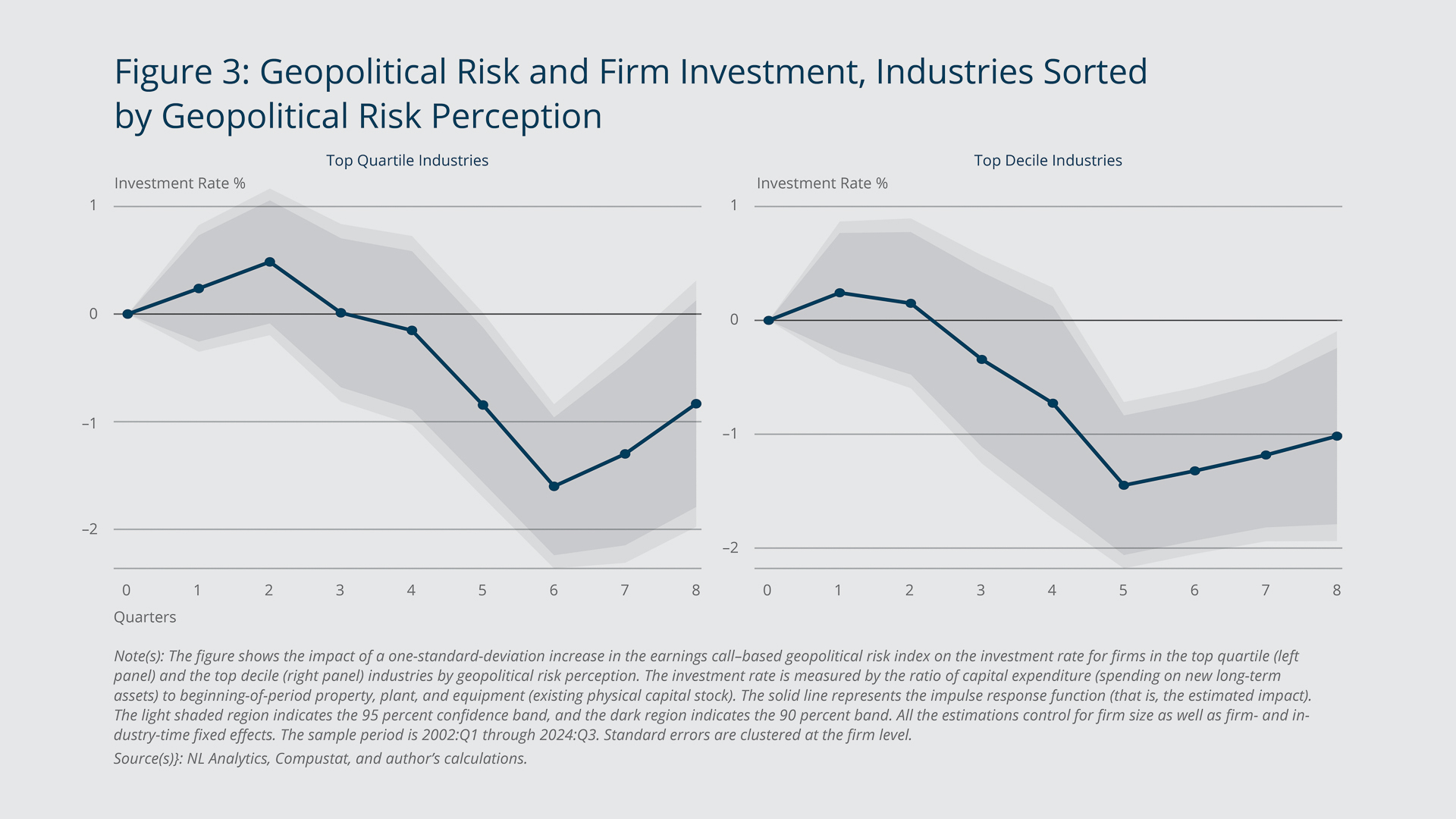

The left panel of Figure 3 shows the effect of a one-standard-deviation increase in the geopolitical risk index on firm investment for industries in the top quartile of geopolitical risk perception over an eight-quarter horizon. I measure investment by the ratio of capital expenditure (a standard measure of firms’ spending on new long-term assets) to beginning-of-period property, plant, and equipment (a standard measure of firms’ existing physical capital stock), controlling for firm size as well as firm- and industry-time fixed effects. As the figure shows, a one-standard-deviation increase in the geopolitical risk index leads to a 1 percent decline in the investment rate after five quarters and a 1.6 percent decline after six quarters for firms in the top quartile of industries by geopolitical risk perception.

{kind=link}

Federal Reserve Bank of Boston

This effect manifests earlier and is more prolonged as, according to firms’ perceptions, geopolitical risk increases. The right panel of Figure 3 illustrates the impact of a one-standard-deviation increase in the geopolitical risk index on firm investment for industries in the top decile by risk perception each quarter. For these firms, a one-standard-deviation increase in the index leads to a 0.7 percent decline in the investment rate after four quarters and a 1.4 percent decline after five quarters.

{kind=link}

Federal Reserve Bank of Boston

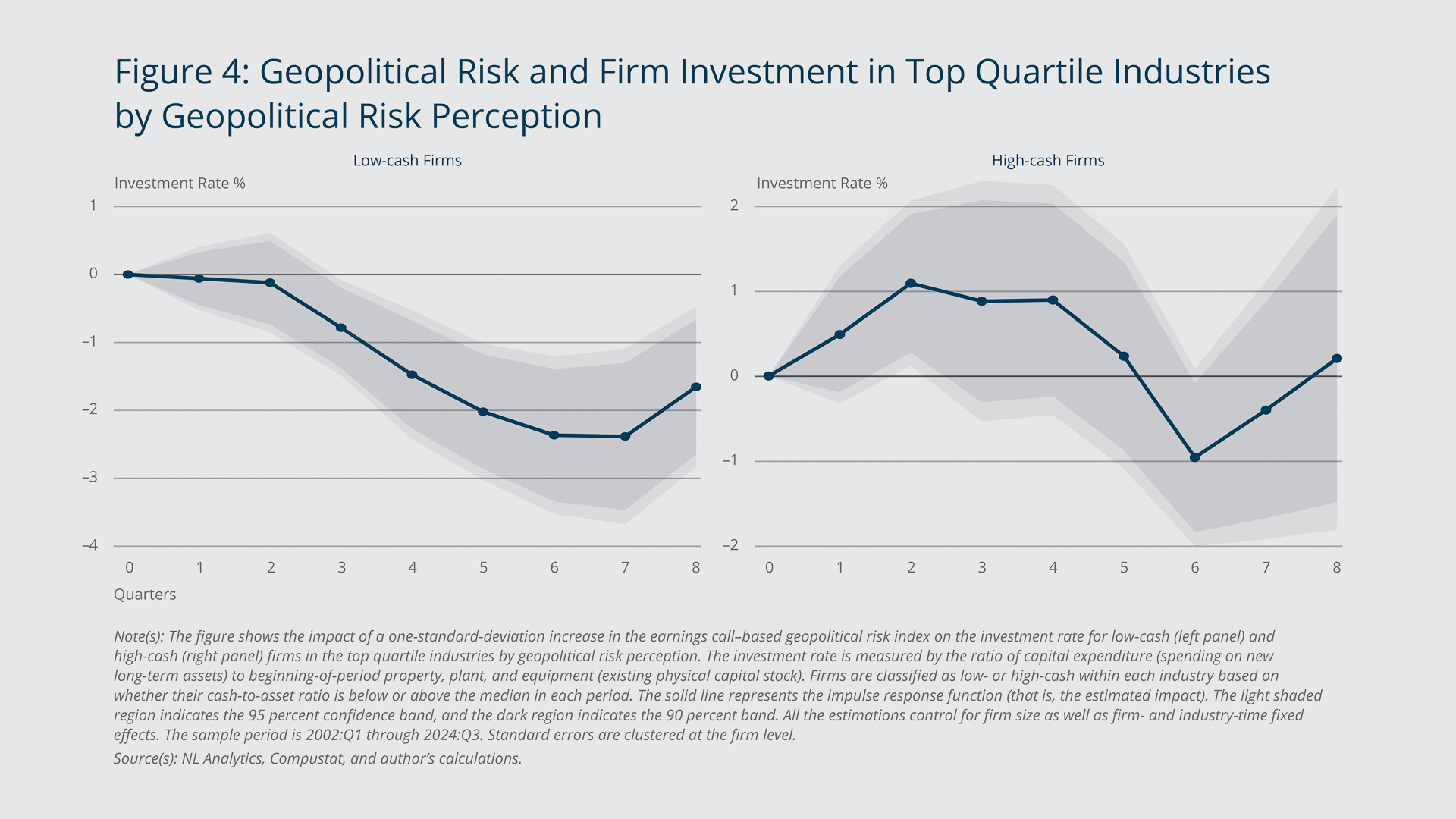

I also find that the impact of geopolitical risk on investment depends on firms’ cash holdings, as cash could act as a cushion to absorb large shocks. I classify firms within each industry as low- or high-cash based on whether their cash-to-asset ratio is below or above the median in each period. Figure 4 shows the impact of a one-standard-deviation increase in the geopolitical risk index on firm investment for low-cash (left panel) and high-cash (right panel) firms in industries in the top quartile of risk perception over an eight-quarter horizon. Evidently, geopolitical risk leads to a significant and persistent reduction in future investment for firms with low-cash positions, while the effect is insignificant for high-cash firms.

These findings, together with the results concerning firms in high-risk-index industries, highlight the potential of geopolitical risk perceptions weakening demand and disrupting the real economy.

Endnotes

- Caldara and Iacoviello (2022) define geopolitical risk as “the threat, realization, and escalation of adverse events associated with wars, terrorism, and any tensions among states and political actors that affect the peaceful course of international relations” (p. 1197). In that paper, they introduce a geopolitical risk index based on the content of newspaper articles. Their index spiked in March 2022, following Russia’s invasion of Ukraine, reaching its highest level in more than 20 years, and it has remained elevated relative to the last two decades (see https://www.matteoiacoviello.com/gpr.htm).

- In contemporaneous work, Niepmann and Shen (2024) construct a country-specific geopolitical risk index from earnings call transcripts using the same method.

- When a set of values is standardized, the mean is zero and the standard deviation from the mean is one.

References

Caldara, Dario, and Matteo Iacoviello. 2022. “Measuring Geopolitical Risk.” American Economic Review 112(4): 1194–1225. https://doi.org/10.1257/aer.20191823

Hassan, Tarek A., Stephan Hollander, Laurence van Lent, and Ahmed Tahoun. 2019. “Firm-level Political Risk: Measurement and Effects.” The Quarterly Journal of Economics 134(4): 2135–2202. https://doi.org/10.1093/qje/qjz021

Jordà, Òscar. 2005. “Estimation and Inference of Impulse Responses by Local Projections.” American Economic Review 95(1): 161–182. https://doi.org/10.1257/0002828053828518

Montiel Olea, J. L., and M. Plagborg-Møller. 2021. “Local Projection Inference Is Simpler and More Robust Than You Think.” Econometrica, 89(4): 1789–1823. https://doi.org/10.3982/ECTA18756

Niepmann, Friederike, and Leslie Sheng Shen. 2024. “Geopolitical Risk and Global Banking.” Working Paper.

About the Authors

About the Authors

Leslie Sheng Shen,

Federal Reserve Bank of Boston

Leslie Sheng Shen is a senior economist in the Federal Reserve Bank of Boston Research Department.

Email: LeslieSheng.Shen@bos.frb.org

Acknowledgments

Cole Kurokawa and David Schramm provided outstanding research assistance and data support.

Resources

Site Topics

Keywords

- geopolitical risk ,

- firm investment ,

- cash position

JEL Codes

- D8 ,

- E22 ,

- G30

Citation

Shen, Leslie Sheng. 2025. “How Firms’ Perceptions of Geopolitical Risk Affect Investment.” Federal Reserve Bank of Boston Current Policy Perspectives 25-3.