Small and Medium-sized Businesses’ Expectations Concerning Tariffs, Costs, and Prices

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Small and medium-sized businesses (SMBs) constitute an integral part of the US economy, driving job creation and economic growth. They account for approximately half of private-sector employment and play a crucial role in fostering competition, all the while supporting local communities. Yet, little if any research has focused on how SMB decision-makers think about the economy and how policy changes could affect their decisions. We use a survey of SMB decision-makers that we developed to foray into such research.

Our current analysis focuses on potential US tariff changes and how they could affect SMBs’ costs and prices and, in turn, the economy as a whole. The eventual impact of tariffs on prices charged by domestic firms has important implications for the inflation outlook, but it is not yet well understood. Findings from previous studies range from virtually zero to some measurable, though still incomplete, cost pass-through into prices (see Amiti, Redding, and Weinstein 2019 and Cavallo et al. 2021). A key component of our survey is a randomized controlled trial that allows us to isolate the causal effects of tariffs by comparing responses of different groups of firms: those that are randomly selected to receive information about tariffs within the survey and those that are not.

Sign up for Research Department Updates.

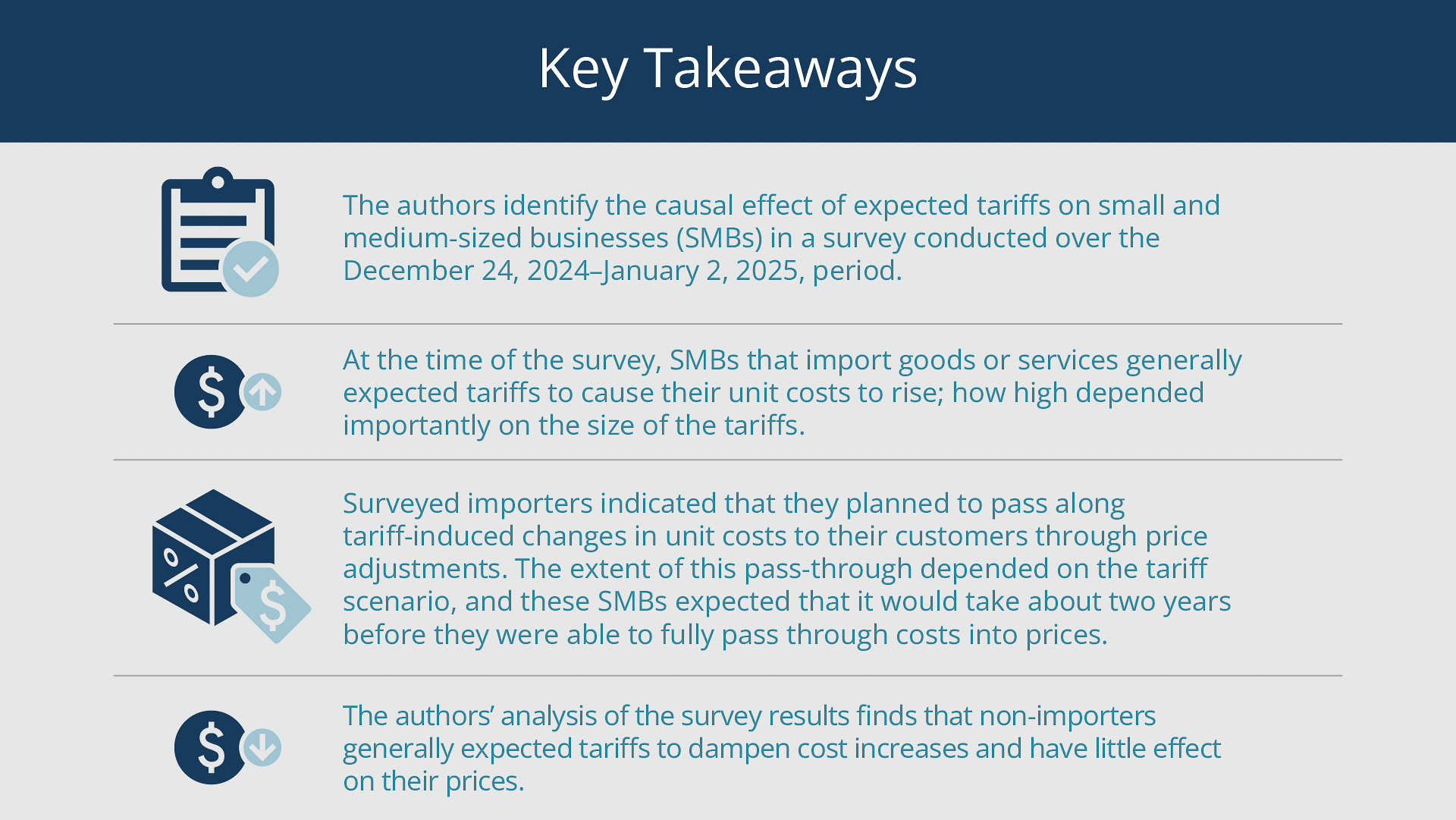

Our analysis produces several insights. First, when the survey was conducted, at end of the fourth quarter of 2024, SMBs expected tariff increases for most US trading partners, but they were uncertain about the ultimate size of the tariffs. Second, firms that import goods or services1 generally expected their unit costs to increase as a result of tariffs; how much they expected costs to rise depended on the particular tariff scenario they were presented in the survey.2 Third, firms planned to pass along the expected tariff-induced changes in unit costs to their customers through price increases; the extent of this cost pass-through would vary under different tariff scenarios.3 They also expected that it would take about two years before they were fully passing through cost increases into prices. Fourth, businesses that noted they do not import expected tariffs to have little effect on their prices and, potentially, a dampening effect on their costs.

New Survey Asked Businesses about Their Tariff Expectations

The new, quarterly survey of US SMBs on which we base our analysis is administered by Morning Consult,4 a US company that specializes in survey research. SMBs are defined as businesses employing 500 or fewer workers. The survey covers a wide range of variables pertaining to firm-level outcomes and plans, such as costs, prices, revenues, profitability, and sourcing of inputs (the resources, including labor and capital, used to produce goods and services). It queries the decision-makers at 500 to 600 firms. We implement additional quality assurance checks and use appropriate statistical techniques to ensure that the sample of businesses in the survey is nationally representative of all SMBs in the United States. (See the accompanying appendix for details.) Our analysis is based on the resulting sample of 444 firms in the 2024:Q4 survey, which Morning Consult conducted over the period of December 24, 2024, through January 2, 2025.

Decision-makers’ responses to two sets of tariff-related questions form the basis for our study. The first set asked about the tariff rates they expected for 2025, distinguishing between imports from Canada, Mexico, China, Europe, and Asian countries other than China. In particular, for each of those countries or regions, they were asked, “In 2025, tariffs may increase for many imported goods and services. How high do you think the new tariffs will be? Please indicate your answers in percent.”

The survey then randomly presented one of three different tariff scenarios to a subset of firms. One group of firms in the subset was told that tariffs on many goods and services could be about 10 percent, while another group was informed that tariffs could be about 25 percent. The third group was told that the tariffs could be about 10 percent, but the group also was told that it was currently highly uncertain how large the tariffs ultimately would be. The remaining firms—the ones not included in the tariff-scenarios subset—were given no additional information about tariffs. They serve as the control group.

Each survey participant then reported their expectations regarding costs and prices for their firm for the next six months, one year, and two years. The firms that received information about potential tariffs presumably reported expectations that incorporated such information. Because some firms randomly received information about tariffs, while others did not, our analysis can gauge the causal effect of each expected tariff scenario on key SMB economic variables, including costs and prices.

Businesses Were Generally Expecting Tariffs Increases, but They Were Not Sure How Large They Would Be

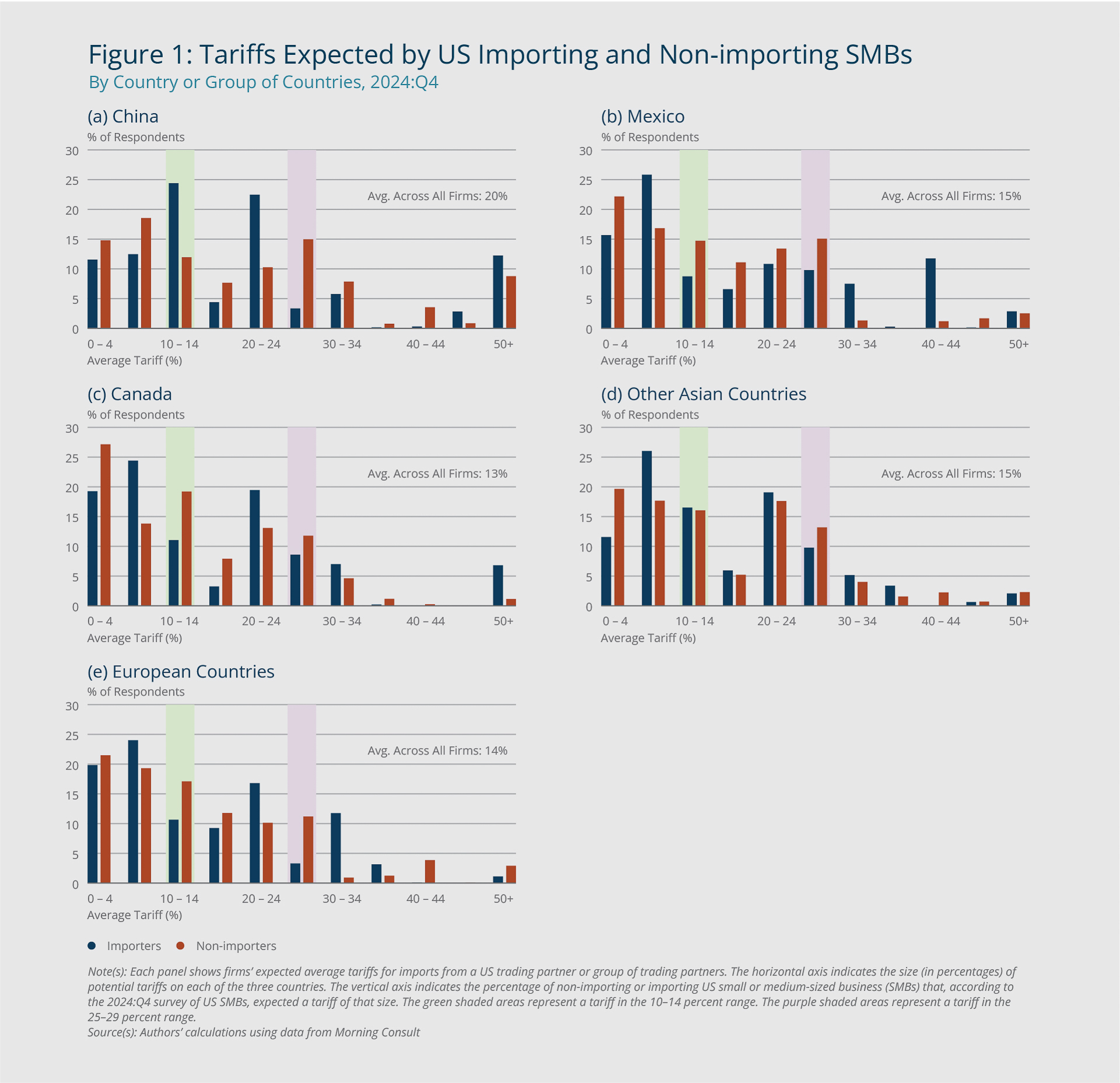

At the time of the survey, SMBs expected tariff increases for most US trading partners, particularly China and other Asian countries, but they were uncertain about the ultimate size of the tariffs. Figure 1 shows the distribution of expected US tariffs for major US trading partners: Canada, China, Mexico, other Asian countries, and European countries. While the survey responses varied widely—potentially reflecting firms’ uncertainty about policy changes—on average, SMBs at the time of the survey (as noted, at the end of 2024:Q4) expected new tariffs on imports from China of about 20 percent (panel a), 15 percent on imports from Mexico (panel b), close to 13 percent on imports from Canada (panel c), 15 percent from other Asian countries (panel d), and 14 percent from European countries (panel e).

{kind=link}

Federal Reserve Bank of Boston

Notably, as our analysis further shows, while the average expected tariff was higher than the existing levels at the turn of the year, almost 40 percent of SMBs expected that tariffs would ultimately be 10 percent or less across all US trading partners, and nearly one-fifth anticipated that they would be 5 percent or less, reflecting a wide range of expected tariffs across firms.

The firms were also asked to state the minimum and maximum tariffs that they expected, allowing us to gauge their uncertainty about future trade policy decisions. As Figure 2 shows, there was a positive correlation between SMBs’ uncertainty—represented by the size of the range of possible tariffs (the vertical axis)—and the expected size of tariffs (the horizontal axis): The SMBs that expected the highest tariffs were also the most uncertain about their size.

{kind=link}

Federal Reserve Bank of Boston

Importers Expected Cost Increases; Non-importers Did Not

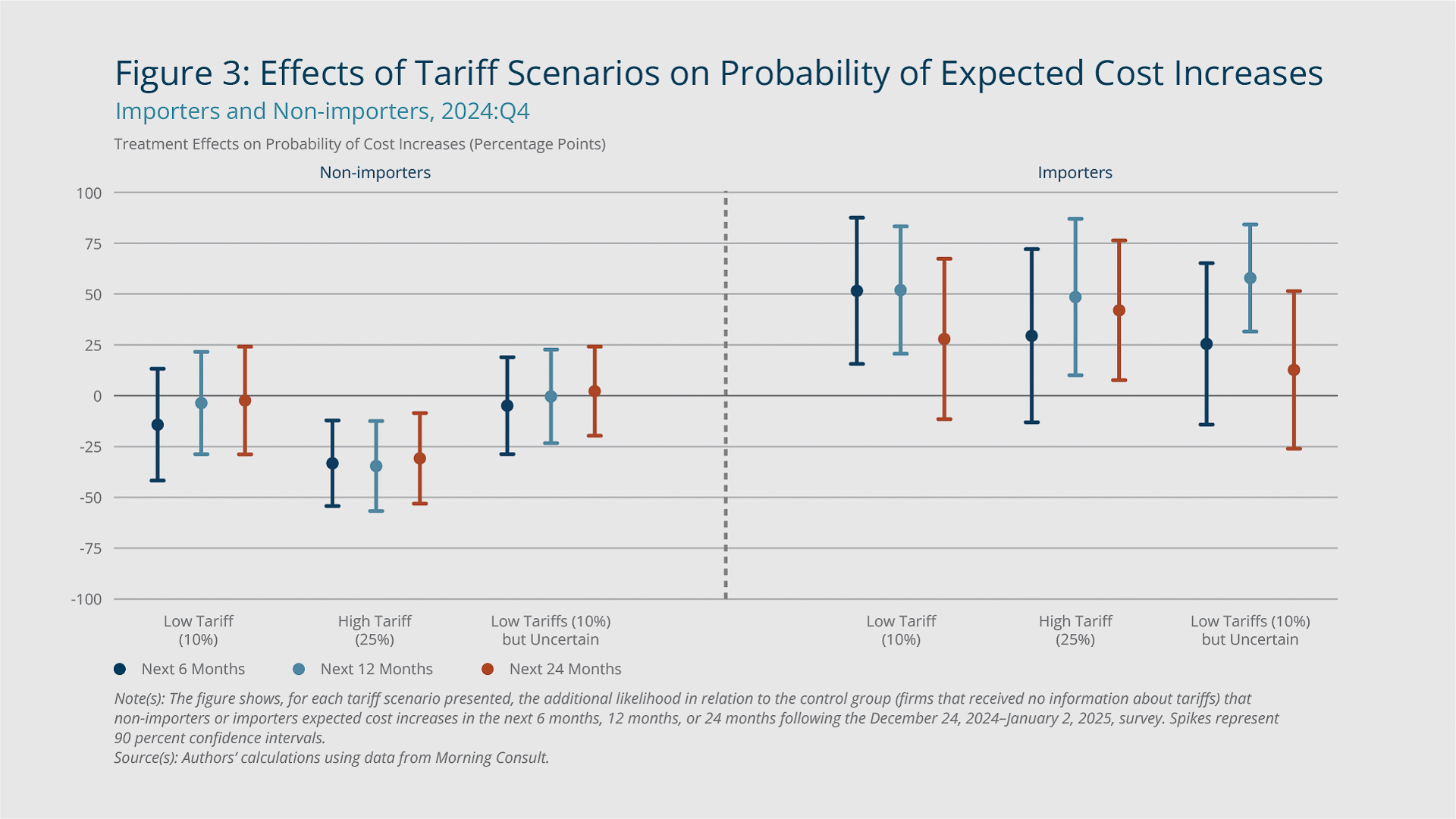

The survey’s randomly assigned tariff scenarios—tariffs of 10 percent, 25 percent, or 10 percent but with high uncertainty—led to different responses from the SMBs, particularly among the importers, which make up about 17 percent of our sample. We use this exogenous variation to study how firms expected tariff changes to causally affect their unit costs and other outcomes.

To start with, we examine the effect of expected tariffs on the likelihood that firms reported higher expected costs. Figure 3 shows that SMBs that import goods or services were significantly more likely than non-importing SMBs to have reported that they expected cost increases as a result of tariffs. Importers that were presented with any of the three tariff scenarios were close to 50 percentage points more likely to report that they expected cost increases over the following year compared with importers in the control group. We do not find that result among the firms that do not import. In fact, under the 25 percent tariff scenario, non-importing firms actually tended to be significantly less likely to expect cost increases.

{kind=link}

Federal Reserve Bank of Boston

Figure 4 further shows that under any of the tariff scenarios presented to survey participants, importers expected their costs would be more than 1.5 percentage points higher in one year. By contrast, firms that do not import expected their costs to decline as a result of tariffs, particularly after longer periods; non-importers presented with the scenario of 25 percent tariffs expected their costs to be as much as 3.6 percentage points lower after two years.

{kind=link}

Federal Reserve Bank of Boston

The reason for this expected decline in costs is unclear. One of many potential explanations could be that, at the time of the survey, non-importing firms believed tariffs could reduce aggregate demand and therefore ease price pressures on inputs such as raw materials or labor costs. Another may be that the non-importers perceived that tariffs would improve business conditions in the United States in general, for instance, by favorably affecting costs.

Importers Expected to Pass Through Cost Increases into Prices over the Next Two Years

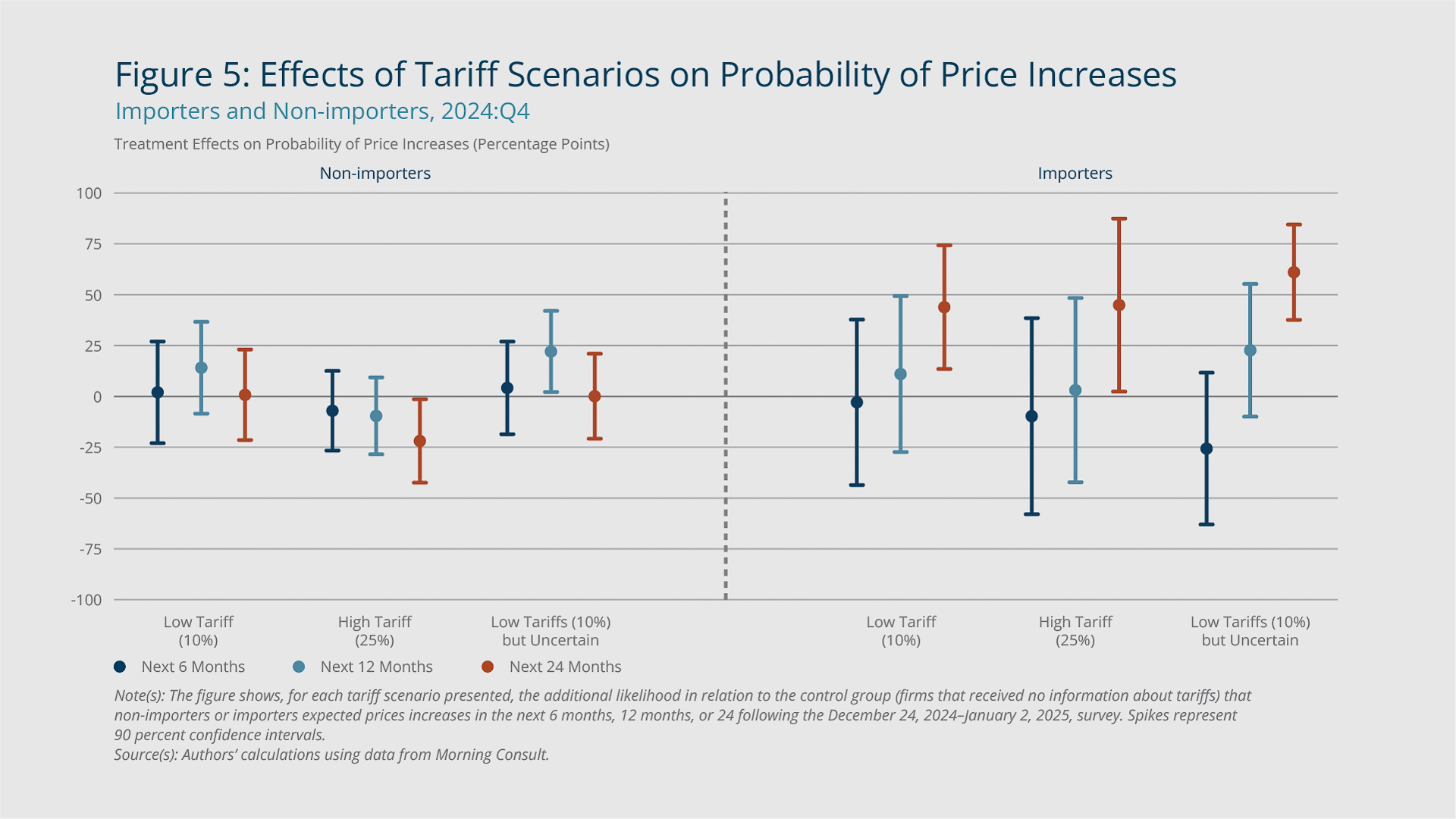

We take our analysis a step further and measure the degree to which SMBs expected tariffs to pass through to their customers through higher prices. As with costs, we first examine the effect of each tariff scenario on whether firms expected price increases. Figure 5 shows that, relative to the control group, importers were more likely to expect price increases under each tariff scenario. However, unlike with costs, for which they anticipated increases in the first year of new tariffs, importers expected price increases only after two years.

{kind=link}

Federal Reserve Bank of Boston

In general, tariffs had very little effect on whether non-importers expected prices to increase. In fact, non-importers who were presented with the 25 percent tariff scenario where less likely than the control group to expect price increases.

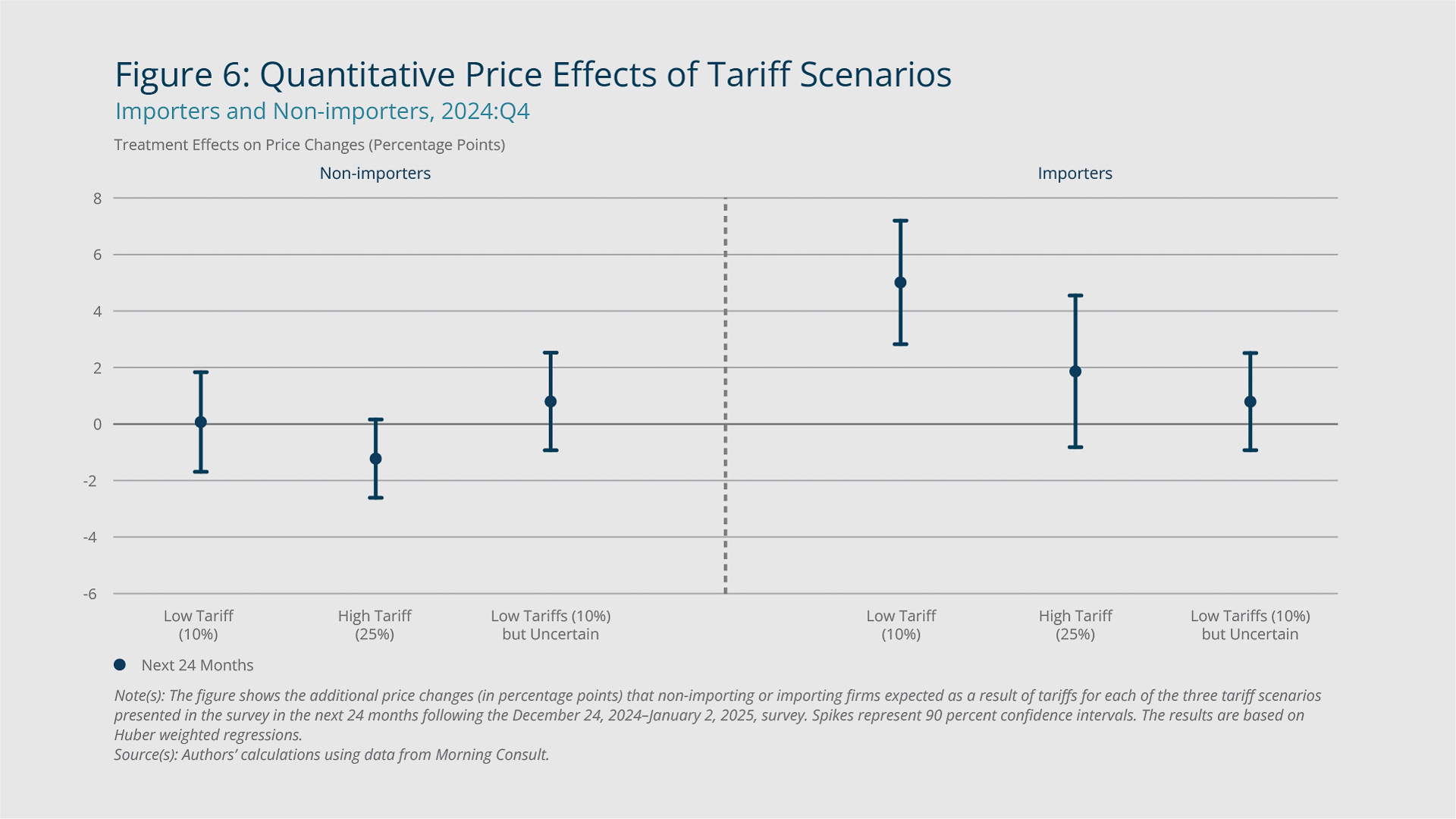

Figure 6 quantifies the two-year expected price changes and shows a range of effects depending on the tariff scenario. With 10 percent tariffs, importers expected prices to increase an additional 5 percentage points over the next two years. Taken together with the cost estimates from the preceding section (3.6 percentage point increase with the 10 percent tariffs), this finding implies that importers expected a more-than-complete pass-through of costs into their customers’ prices in this scenario.

{kind=link}

Federal Reserve Bank of Boston

In the 25 percent tariff scenario and the 10 percent but uncertain tariff scenario, importers expected prices to rise but not as sharply as in the 10 percent tariff scenario. Their expectations imply a partial pass-through of tariffs to their customers and could reflect expected lower demand in the economy due to several possible factors, including high tariffs.

Non-importers who were presented with the 25 percent tariff scenario expected prices to decline about 1 percent as a result of tariffs, whereas non-importers who were presented with the other tariff scenarios did not expect prices to be affected by tariffs.

Endnotes

- Throughout this article, we refer to importers as businesses that state either that they only import or that they both export and import when asked in the survey, “Does your business export goods or services to another country or import goods or services from another country?”

- This finding is consistent with findings in Abel, Deitz, and Hyman (2025), who show that firms that account for large shares of US imports expected greater cost increases from the imposition of additional tariffs.

- This finding is consistent with media reports on how tariff increases could affect consumer prices. See, for example, Jaewon Kang and Lily Meier, “Target, Best Buy Warn US Consumers of Tariff Price Hikes,” Bloomberg News, March 4, 2025.

- See http://morningconsult.com.

References

Abel, Jaison R., Richard Deitz, and Ben Hyman. 2025. “Firms’ Inflation Expectations Have Picked Up.” Federal Reserve Bank of New York Liberty Street Economics (blog). March 5.

Amiti, Mary, Stephen J. Redding, and David E. Weinstein. 2019. “The Impact of the 2018 Tariffs on Prices and Welfare.” Journal of Economic Perspectives 33(4): 187–210. https://doi.org/10.1257/jep.33.4.187

Cavallo, Alberto, Gita Gopinath, Brent Neiman, and Jenny Tang. 2021. “Tariff Pass-through at the Border and at the Store: Evidence from US Trade Policy.” American Economic Review: Insights 3(1): 19–34. https://doi.org/10.1257/aeri.20190536

About the Authors

About the Authors

Philippe Andrade,

Federal Reserve Bank of Boston

Philippe Andrade is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Philippe.Andrade@bos.frb.org

Alexander M. Dietrich is a research economist in the Danmarks Nationalbank Research Unit.

John Leer is the chief economist at Morning Consult.

Raphael S. Schoenle,

Federal Reserve Bank of Boston

Raphael S. Schoenle is a professor of economics at Brandeis University and a visiting scholar in the Federal Reserve Bank of Boston Research Department.

Jenny Tang,

Federal Reserve Bank of Boston

Jenny Tang is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Jenny.Tang@bos.frb.org

Egon Zakrajšek,

Federal Reserve Bank of Boston

Egon Zakrajšek is an executive vice president at the Federal Reserve Bank of Boston and the director of the Research Department.

Email: Egon.Zakrajsek@bos.frb.org

Acknowledgments

The authors thank Ara Patvakanian and David Brown for excellent assistance on the data and figures.

Resources

Site Topics

Keywords

- business expectations ,

- Surveys ,

- tariffs ,

- cost pass-through ,

- inflation

JEL Codes

- E31 ,

- F13 ,

- F14 ,

- F40 ,

- C83

Citation

Andrade, Philippe, Alexander M. Dietrich, John Leer, Raphael S. Schoenle, Jenny Tang, and Egon Zakrajšek. 2025. “Small and Medium-sized Businesses' Expectations Concerning Tariffs, Costs, and Prices.” Federal Reserve Bank of Boston Current Policy Perspectives No. 25-7.

Related Content

2015 Small Business Credit Survey

Distributional Effects of Payment Card Pricing and Merchant Cost Pass-through in the United States and Canada

How Small is Zero Price? The True Value of Free Products

Informational Session to Understand the Small Business Investment Company (SBIC Program)