Evidence That Relaxing Dealers’ Risk Constraints Can Make the Treasury Market More Liquid

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

The market for US Treasury securities is a crucial component of the global financial system, representing more than $33 trillion in debt outstanding at the end of 2023. Not only are Treasury securities—or, Treasuries—the primary means of financing the US federal government, but they are also a significant investment instrument and hedging vehicle for domestic and international investors and serve as a risk-free benchmark for many other financial instruments, such as corporate bonds and mortgages. Treasuries are also essential for the Federal Reserve’s monetary policy implementation and transmission to the broader economy.1

However, despite its size and importance, the Treasury market is intermediated by a small group of market-making financial firms—typically affiliated with large banking organizations.2 These so-called primary dealers acquire Treasuries directly from the US government as it issues new debt through auctions in what is known as the primary market. The primary dealers then resell the Treasuries to investors in the secondary market. Primary dealers are also direct business counterparties to the Federal Reserve’s monetary policy operations, meaning they trade securities with the Fed.

Sign up for Research Department Updates.

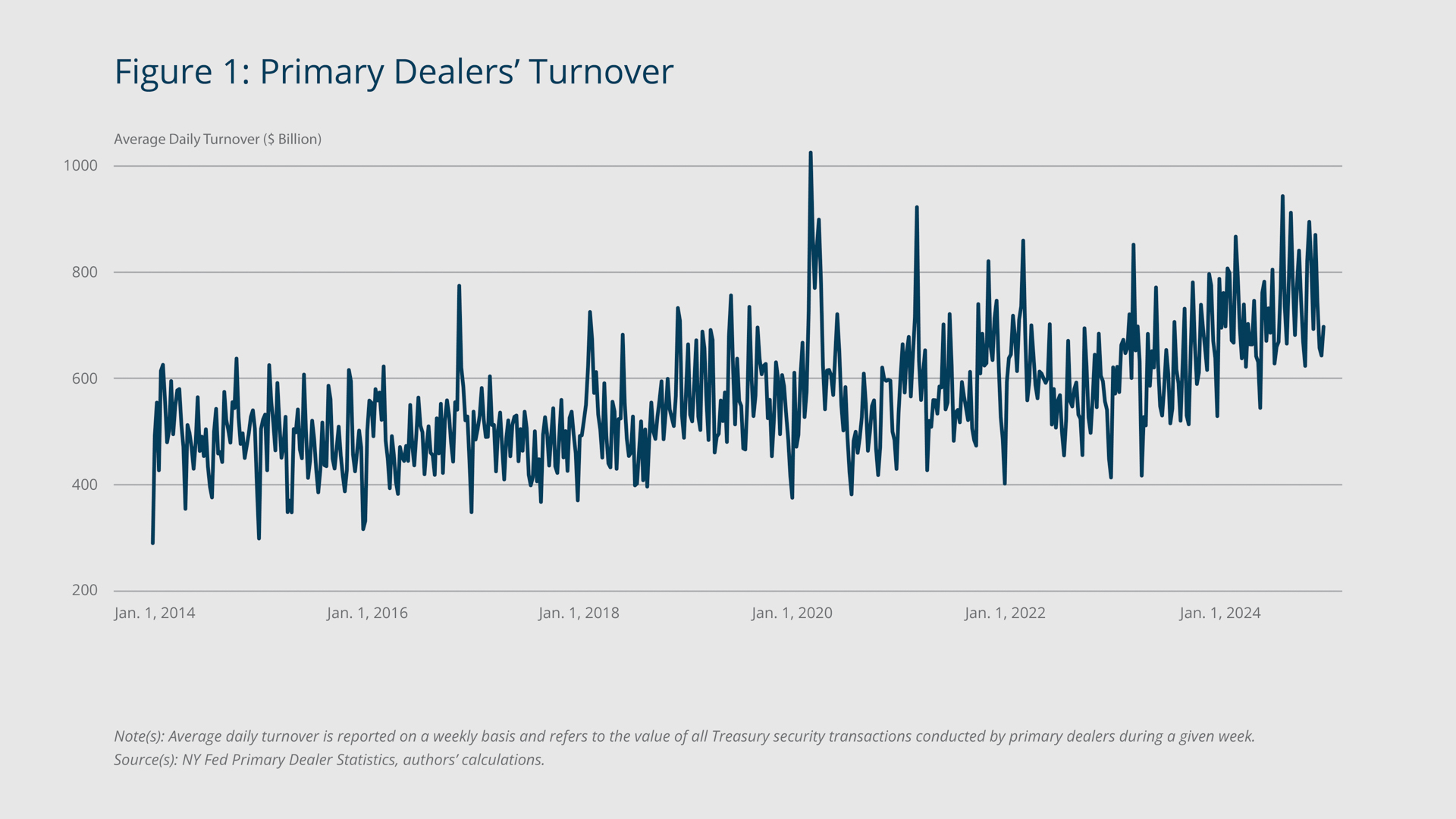

Figure 1 indicates the substantial size of primary dealers’ footprint in the Treasury market: Their average daily turnover (the volume of Treasuries they traded) each week ranged from $545 billion to $944 billion in 2024. Given the crucial role of primary dealers, policymakers and academics have pointed out the potential vulnerability of the Treasury market to changes in constraints on those dealers—such as changes involving banking capital regulation—that would affect their ability to efficiently intermediate the market (see, for example, Duffie 2018, 2020). This discussion has gained momentum in the wake of several recent disruptions in the Treasury market, significant accumulation of government debt in response to the COVID-19 crisis, and projections of further increasing federal deficits.3

{kind=link}

Federal Reserve Bank of Boston

This brief studies how regulation involving bank capital requirements affects the behavior of bank-affiliated primary dealers in the Treasury market. Specifically, it looks at the potential effects of changes to the supplementary leverage ratio (SLR) requirement, which determines how much capital a bank must hold in relation to its overall exposure, including exposure in its trading assets such as Treasuries. The SLR is a measure of a bank’s ability to absorb losses during periods of financial stress; the Federal Reserve sets a minimum requirement for the SLR to help protect the stability of the banking system by preventing excessive leverage. Our analysis presents evidence that relaxing the SLR constraint—that is, lowering the required SLR—can cause an increase in dealers’ Treasury trading activity, especially among dealers affiliated with more constrained (lower-SLR) banks. This finding implies that the SLR requirement is indeed binding for some banks—that it constrains their Treasury positions to levels they would not otherwise choose.

When Banks’ SLRs Rose, Treasury Market Liquidity Improved

The SLR requirement represents the US implementation of the leverage ratio outlined in the Basel III accords.4 It applies generally to large banks with more than $250 billion in total consolidated assets. Current regulation requires that these banks’ Tier 1 capital amounts to 3 percent of their total leverage exposure.5 Importantly, total leverage exposure includes primary dealers’ gross positions in securities: the sum of their long positions (the value of securities owned) and short positions (the value of securities they have promised to deliver).

Banks that are constrained by the SLR requirement may have to reduce their trading assets or may not be able to expand them, potentially weakening their market-making role and impairing Treasury market liquidity.

This brief identifies the effect of the SLR requirement on the Treasury market using an unexpected policy change during a crisis period. At the onset of the COVID-19 pandemic, the Treasury market was severely strained with low liquidity and high volatility. In response, the Federal Reserve Board announced, on April 1, 2020, a temporary exemption of Treasuries and reserves from the SLR requirement, meaning Treasury holdings would not factor into a bank’s SLR calculation. This unanticipated policy change became effective immediately and lasted through March 31, 2021. The stated objective was “to ease strains in the Treasury market resulting from the coronavirus [...].”6 The policy change effectively increased banks’ SLRs and freed up balance sheet space that could be used for holding Treasuries and increasing trading activity.

{kind=link}

Federal Reserve Bank of Boston

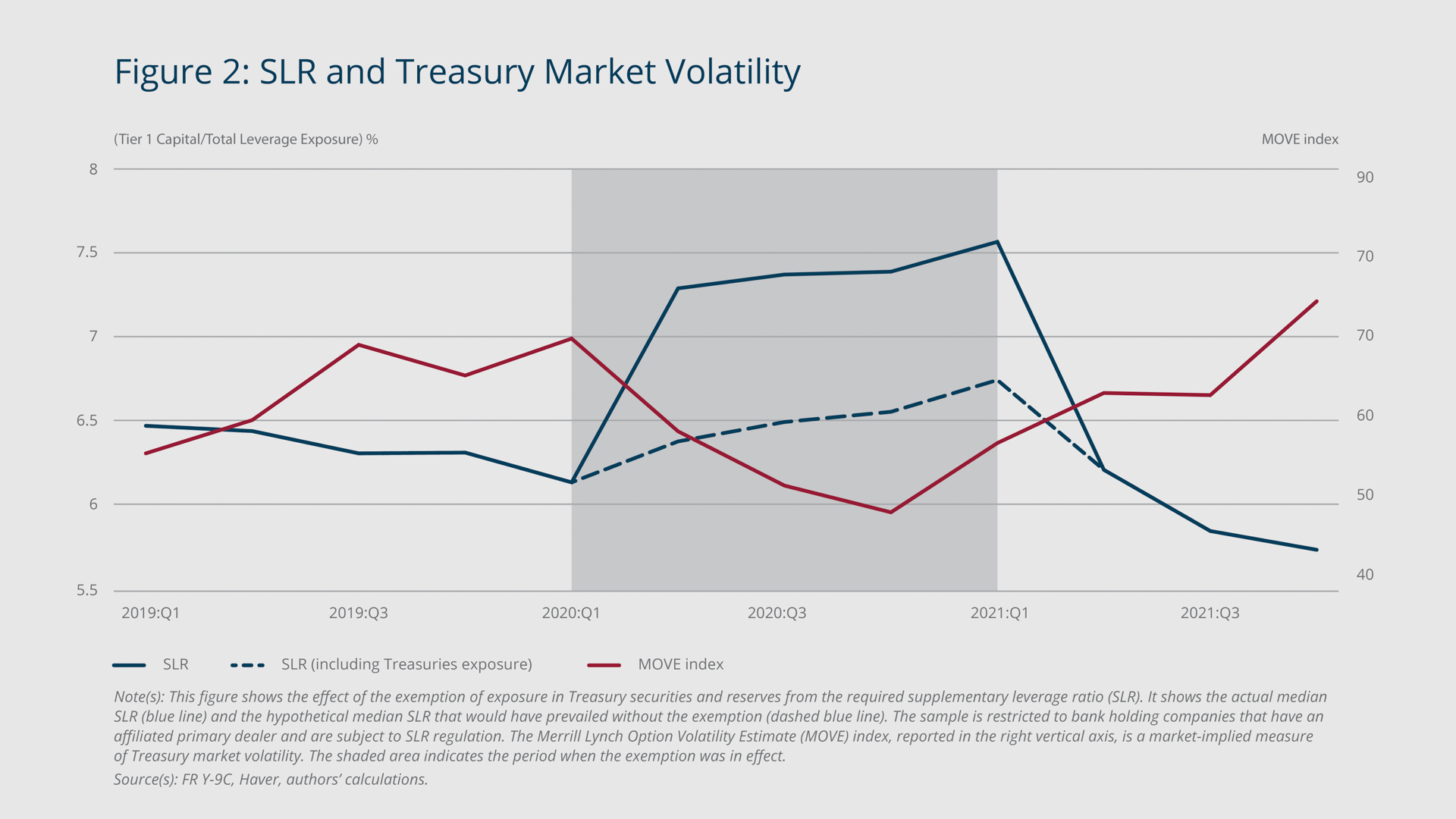

Figure 2 shows the impact of the temporary exemption on banks’ median SLR and on the Merrill Lynch Option Volatility Estimate (MOVE) index, an indicator of Treasury market volatility and liquidity. The policy change boosted the median SLR by more than 1 percentage point relative to both the pre-change level and the counterfactual median SLR (dashed line) that would have prevailed absent the exemption. Treasury market liquidity improved concurrently with the policy change, as indicated by the decline in the MOVE index. Our analysis digs into this dynamic in more detail and enables us to identify a causal tie between the relaxing of dealer constraints and the improvement in the market’s liquidity.

Lower-SLR Banks Responded More to the Rule Change

Following Bräuning and Stein (2024), this brief zooms in on the effects of the SLR exemption on the Treasury market by using detailed confidential microdata on primary dealers’ weekly positions, turnover, and trading income. These data, known as FR 2004, are collected by the Federal Reserve Bank of New York; data submission is mandatory and required for obtaining primary dealer status.

To show how the SLR exemption caused Treasury market movements, we compare banks’ responses to the exemption based on their SLR before the exemption. In other words, we use a difference-in-differences approach. The idea is that banks with an SLR closer to the minimum ratio before the policy change were more constrained by the regulation than banks with higher SLRs. Therefore, they would have benefited more from the loosening of the requirement and should have made larger adjustments in their Treasury holdings. Because our comparison of banks focuses on weekly activity, the findings do not reflect broader market trends.7

{kind=link}

Federal Reserve Bank of Boston

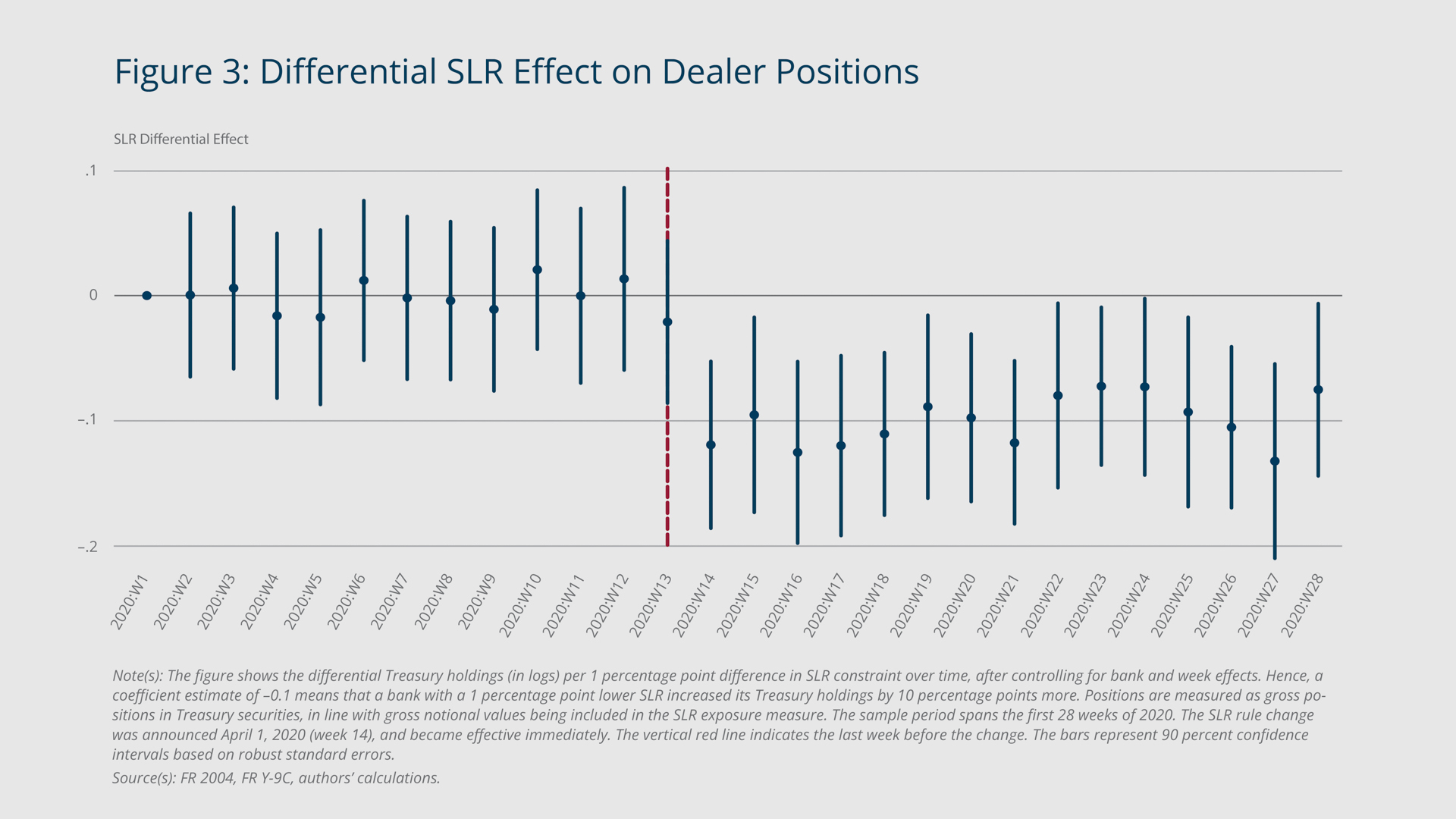

Figure 3 shows how the temporary exemption of Treasuries from banks’ SLRs boosted the holdings of more constrained (lower-SLR) dealers more than those of less-constrained (high-SLR) dealers. When the policy change went into effect on April 1, 2020 (week 14 on the chart), banks increased their Treasury position by about 10 percentage points in the first week for every additional 1 percentage point reduction in SLR constraint. So, for example, on average, a bank with a pre-policy-change SLR of 6 percent increased its Treasury holdings by about 40 percentage points more than a bank with a pre-policy-change SLR of 10 percent.

This effect is economically sizable. In our regression sample, where the average weekly Treasury position per bank is $34.27 billion, our estimate translates into an increase in Treasury positions in the first week by about $3.4 billion for every additional 1 percentage point reduction in SLR constraint. In 2019, before the pandemic and before the policy change, the SLRs of the banks we examine ranged from 5.7 to 12.1 percent, with a mean of 7.1 percent and a standard deviation of 1.9 percent. This translates to sizeable effects on Treasury positions when we compare lower-SLR banks with higher-SLR banks.8

In our estimation, the differential effect remains significant for several weeks, until it decreases and becomes indistinguishable from zero at the end of 2020 (not shown in the figure). Importantly, our analysis finds no differential effect of banks’ SLRs on Treasury trading activity before the policy change, giving us confidence that the policy change is indeed what caused the differential effect between banks.

In this brief’s companion working paper (Bräuning and Stein 2024), we obtain similar results when, instead of using a bank’s pre-policy-change SLR to proxy its constraint, we calculate the increase in each dealer bank’s SLR due to the policy change. The results confirm our key point: The change to the required SLR had a strong impact on dealers’ Treasury positions.

In addition to increasing their Treasury positions after the implementation of the SLR exemption, primary dealers increased their turnover and decreased their profit margin (defined as the ratio of trading income to position size). Specifically, Bräuning and Stein (2024) show that lower-SLR (more constrained) dealers increased their turnover by 7 percentage points and decreased their profit margin by 10 percentage points for every additional 1 percentage point increase in SLR constraint.

As in our analysis on Treasury positions, these effects are highly statistically significant. They are also economically sizeable. The average weekly Treasury position per bank in our regression sample is $209 billion; thus, our estimate implies an increase in Treasury turnover of about $146 billion for every additional 1 percentage point increase in SLR constraint. Similarly, because the average weekly profit margin is 8 basis points, our estimate implies a decrease in profit margin of about 1 basis point for every additional 1 percentage point increase in SLR constraint.

These findings are consistent with models of constrained intermediaries: When constraints are relaxed, banks can hold larger Treasury positions, allowing them to facilitate more turnover—that is, improve the market’s liquidity—by buying Treasuries at higher prices and selling them at lower prices on the secondary market. The improved liquidity is reflected in a narrowing of the intermediation (or, bid–ask) spread—the difference between the highest price Treasury buyers will pay (the bid price) and the lowest price sellers will accept (the ask price).

SLR-constrained Dealers Also Increased Non-Treasury Holdings

The SLR is a risk-insensitive capital ratio, meaning that all securities—including corporate bonds, for example, as well as Treasuries of different maturities—contribute equally to the SLR exposure measure. Therefore, we would expect the policy change to have the same effect on all types of Treasuries, regardless of their risk profile. This is indeed what we find: Although Treasuries with longer maturities are riskier, the policy change did not have a differential effect on the volume that primary dealers traded relative to Treasuries with shorter maturities.

In addition to looking at how primary dealers’ Treasury positions changed after the surprise exemption, we examine their positions in other asset classes. We find that lower-SLR (more constrained) dealers increased their holdings of non-Treasury securities, such as mortgage-back securities (MBS) and corporate bonds, after the policy change. This is in line with an “income effect”: The exemption effectively increased the equity capital available for funding both Treasury and non-Treasury positions.

On the other hand, one could also imagine a “substitution effect,” whereby banks would find it relatively less attractive to hold non-Treasury securities because Treasuries no longer contributed to their SLR and therefore were relatively and absolutely less costly to hold. Because bank holdings of non-Treasury securities increased rather than decreased, our evidence suggests that the income effect from the Treasury exemption dominated the substitution effect.

Endnotes

- Treasuries (also spelled Treasurys) include bills, notes, and bonds, among other types of securities. Because the security types differ in terms of maturities and payout schedules, the term Treasury markets is commonly used. In this report, we use the singular because we consider the Treasury market as a whole.

- We refer to banking organization as “banks” hereafter. We also use the term “banks” to refer to the dealers affiliated with the banks as well as the banks.

- See, for example, Eric Wallerstein, “Why Treasury Auctions Have Wall Street on Edge,” The Wall Street Journal, Dec. 10, 2023. https://www.wsj.com/finance/why-treasury-auctions-have-wall-street-on-edge-8385f15e.

- Basel III is an internationally agreed upon set of measures developed by the Basel Committee on Banking Supervision in response to the 2007–2009 financial crisis. The measures aim to strengthen the regulation, supervision, and risk management of banks. Like all Basel Committee standards, the Basel III standards are minimum requirements that apply to internationally active banks. Members are committed to implementing and applying standards in their jurisdictions within the time frame established by the committee.

- Tier 1 capital is a bank’s core equity capital. Total leverage exposure includes all assets and liabilities of the bank, and it is not risk weighted. More stringent requirements for the largest and most systemically important financial institutions add a capital buffer of 2 percent, raising the SLR requirement to 5 percent.

- See “Federal Reserve Board Announces Temporary Change to Its Supplementary Leverage Ratio Rule to Ease Strains in the Treasury Market Resulting from the Coronavirus and Increase Banking Organizations’ Ability to Provide Credit to Households and Businesses,” Federal Reserve Board of Governors press release, April 1, 2020. https://www.federalreserve.gov/newsevents/pressreleases/bcreg20200401a.htm

- Our analysis requires that the change in the SLR rule was not concurrent with other changes that differentially affected banks’ Treasury trading positions depending on their SLR. The high frequency of the FR 2004 data on dealers’ positions and turnover enables us to mitigate such concerns. Specifically, we can rule out that, during the week of the SLR policy change, other relevant policy changes were announced or implemented, or that any relevant financial market developments or broader economic events occurred. For example, the potentially relevant Primary Dealer Credit Facility (PDCF) was announced on March 17, 2020, and began operating on March 20, two weeks before the change in the SLR rule.

- Our study uses a difference-in-differences approach, meaning we compare positions between banks. The benefit of this approach is that it controls for market developments that affected all banks equally. Because a lot was happening during March and April 2020, this control is important in establishing causality. However, the downside of this approach is that it does not enable us to sum across banks and look at the overall effects on Treasury positions.

References

Bräuning, Falk, and Hillary Stein. 2024. “The Effect of Primary Dealer Constraints on Intermediation in the Treasury Market.” Federal Reserve Bank of Boston Research Department Working Papers No. 24-7. https://doi.org/10.29412/res.wp.2024.07

Duffie, Darrell. 2018. “Financial Regulatory Reform after the Crisis: An Assessment.” Management Science 64(10): 4835–4857. https://doi.org/10.1287/mnsc.2017.2768

Duffie, Darrell. 2020. “Still the World’s Safe Haven? Redesigning the U.S. Treasury Market after the COVID-19 Crisis.” Brookings Hutchins Center Working Paper.

About the Authors

About the Authors

Falk Bräuning,

Federal Reserve Bank of Boston

Email: falk.braeuning@bos.frb.org

Hillary Stein,

Federal Reserve Bank of Boston

Email: hillary.stein@bos.frb.org

Resources

Site Topics

Keywords

- supplementary leverage ratio ,

- treasury market liquidity ,

- banking capital regulation ,

- Primary dealers ,

- Intermediation ,

- risk constraints

JEL Codes

- G10 ,

- G12 ,

- G18 ,

- G21

Citation

Bräuning, Falk and Hillary Stein. 2025. “Evidence That Relaxing Dealers’ Risk Constraints Can Make the Treasury Market More Liquid.” Federal Reserve Bank of Boston Current Policy Perspectives 25-4.

Related Content

Dealer Risk Limits and Currency Returns

Real Effects of Foreign Exchange Risk Migration: Evidence from Matched Firm-Bank Microdata

Technology, the Nature of Information, and FinTech Marketplace Lending

Money Market Mutual Funds and Financial Stability